Bank partnerships with Fintechs - Win Win like never before! | Episode #27

The Bank-Fintech relationship in India continues to evolve – COVID appears to have pushed them more towards co-existence as both feed off each other’s strengths

While talking with Nikhil and Ankush from Piggy, one of the most exciting full stack digital banking solution providers, what intrigued me the most was our discussion around the pace at which traditional banks are forming partnerships with fintech! They have taken the bull by horns and if there is one set of player who are really riding the fintech wave, it’s them.

Interestingly, founders in the B2B space such as Dice has been talking about how Open and Zeta grew their businesses multi-fold with the right kind of bank partnerships and how they are following a similar strategy. Overall, what initially looked like an area ripe for competition, has turned into a very synergistic, very collaborative play.

Some of the key areas where Bank-Fintech collaborations seem most prominent are in lending channels, payments, Neobanking, Wealth management and customer experience (CX). In this episode, we will look at key fintech partnerships that some of the most active banks in the country has and also talk about fintechs which are set to ride on top of banking.

Note – In case you are a fintech founder, looking to raise funds, I might be able to help. Reach out to abhishek@indiafintech.in. In case you are looking to invest in Indian Fintech, reach out. Would be happy to help.

What has been happening in the space?

The pandemic has made it necessary for banks to build digital customer acquisition channels and build digital retention channels.

It became necessary not only to onboard customers digitally but also address customer queries and enable transactions online. Digital infra also helps create better customer experience, which is why many Fintech partnerships are being built.

Some of the features banks have partnered with Fintechs on are: i) Chatbots: Fintechs have created chatbots on banks’ platforms, social media and mobile apps to answer customer queries and to perform simple transactions and bill payments, ii) Wealth mgmt: Fintech partnerships also help banks co-create and offer wealth mgmt products, iii) Data Analytics: with fintech expertise in data analytics, banks are able to execute better risk monitoring and fraud protection, and iv) with fintech partnerships banks are also building features like digital payments for SMEs and expense trackers.

Who are the banks driving fintech partnerships?

Big five private sector banks (HDFCB, ICICIB, Axis, Kotak, Federal) are more aggressive in building Fintech partnerships compared to the smaller banks and PSBs. Big five private banks are also seen to hold stakes in Fintechs in the form of strategic/financial investments to grow together with promising Fintechs. This has been getting more and more interesting when banks are coming in at Pre-Series A stage as strategic investors (For e.g. Open, Zeta) driving growth at a much faster pace.

Bank- Fintech partnerships are expected to help provide a richer digital experience and more value added services to attract a growing millennial and mobile first population.

Off late, Yes Bank also seems to be getting in the action and are looking at strategic to drive customer retention. See them partnering with exciting B2B2C digital banks early on.

The following shows partnerships for top banks across fintech segments. Lending and payments are the areas where everyone is present. Neobanks, for all the noise around this, is still shaping up and there are opportunities for both fintechs and banks to form partnerships. Wealth is one super underpenetrated area and I do so some partnerships being formed, soon.

What I have not listed down here are B2B SaaS+Fintech kind of partnerships, which are in super early stages. See many players, including the likes of Dice going big here with larger banks.

In terms of banks, interestingly, Axis Banks seems to be the most active across the spectrum! I wouldn’t have guessed that. And contrary to Axis, the most lethargic one, which everyone would have guessed, is, well, SBI. No surprises there.

Payments and Lending seeing maximum traction

The maximum investments by banks are seen into startups in the payments and lending space. This is because of the large sizes of these two opportunities and the ability of Banks to benefit the Fintechs through their payments channels and as loan originators, while fintechs can bring differentiation through better customer platforms and new age underwriting engines, expanding reach. However, slightly more niche spaces like wealth, neobanks and digital analytics are also seeing some traction.

Enable alternative payment method: Digital payments got a further push from the pandemic- as they became necessary for running most economic activities. This growing relevance of digital payments has helped pave the way for banks to collaborate with Fintechs in order to create a seamless digital payments experience. Banks also partner with Fintechs to better execute cross border remittances.

Offer loans on Fintech platforms: Through Fintech partnerships, banks are trying to expand their digital touchpoints, with Fintechs helping distribute their loans. There are various Fintech models in this space- i) while some Fintechs help banks unlock features for customers such as to get EMI on debit cards or when purchasing with Fintech partnered e-com merchants, and ii) other Fintech models enable distribute loans faster with their algorithms, specialized in assessing credit worthiness of customers with minimum documentation required in as less as 90 seconds.

Some of the larger banks partnerships are across the spectrum and we dive deeper into the top banks partnerships.

Axis Bank

As observed earlier, Axis Bank has really taken the fintech bulls by their horns. They acquired Freecharge (And subsequently offloaded) when no other bank was even deliberating getting into the space.

For E-commerce- Axis has a co-branded credit card with Flipkart, which was launched in 2019. With the credit card consumers get the highest cashbacks across Flipkart, Myntra, 2GUD, and additional benefits across 3rd party merchants such as MakeMyTrip, Goibibo, Uber, PVR, Gaana, Curefit, UrbanClap.

On the lending front, Axis has tied up with Rupifi to provide business credit cards for small businesses through the Rupifi platform. Rupifi works with large aggregators like food delivery, e-commerce, grocery platforms etc. to reach out to micro businesses selling on their platforms. They underwrite these companies on the basis of transaction data and extend credit to them. With the credit card, Rupifi and Axis Bank can extend business loans to these entities through the card.

Axis also has a partnership with Neobank InstantPay, through which it intends to provide and enhanced user experience. Axis Bank customers can open a digital account with InstantPay as an alternative to wallets and traditional bank accounts. Startups and SME businesses can open a Smart Bank Account. They also offer InstantPay Digi Kendra service-which offers basic banking, insurance, and travel booking facilities, among others.

On the payments front, Axis is in partnership with GooglePay and PhonePe on the UPI payments front, while it has partnered with Ripple to offer instant international payments services. Ripple has an enterprise blockchain technology solution, which makes international remittances faster and transparent for customers while ensuring security and improving efficiencies. T

Interestingly, through its partnership with Thales and Tappy Technologies, Axis is offering wearable technologies. The bank’s Wear ‘n’ Pay range includes wristbands, keyrings and watch straps as well as devices that can be incorporated into existing accessories.

Following lists down all fintech parternships for Axis Bank - A super interesting list.

HDFC Bank

HDFC Bank has a good line up of digital partnerships- with most partnerships on payment and User experience front.

On the lending side, HDFC has gone into partnerships to improve sourcing from digital channels– PaisaBazaar and Square Capital on the lending front. With Paisabazaar, HDFC has been working to enable an efficient system to source and lend to customers using tech and innovation. Square Capital, which is the financial management arm of Square Yard, with whom HDFC has partnered for loan disbursals via their website.

On the payments front some of the key partnerships that HDFC Bank has include Google Pay and MobME on the UPI front, Ripple that facilitates cross border payments, Visa/Digitsecure to enable NFC payments and Cashfree to facilitate bulk transactions for enterprises.

HDFC Bank also has tie-ups with tracking apps like Hylo- for SMEs, which gives real-time visibility on the cash or cheque collection done by field agents,bringing greater transparency amongst sellers and buyers.

HDFC Bank has partnered with Niki.ai to create HDFC Bank OnChat- a Facebook Messenger chat service to avail all the bank’s services. The bank also partnered with Salesforth, to create their AI powered chatbot EVA which interacts with users in natural human language. The bot is not only programmed to handle general user queries but also provide product recommendations, instantaneously.

On the wealth front, HDFC Bank has recently entered into an equity investment into Smallcase Technologies- the bank invested an undisclosed amount as part of the fintech startup’s $14 mn Series B fund raise. Smallcase Technologies operates in the capital markets infrastructure space and works with businesses to help individuals invest in simple and transparent products called smallcases.

Following lists down all fintech partnerships for HDFC Bank -

ICICI Bank

ICICI bank is probably one of the most digital focused banks, from what I can learn form friends working in ICICI product team. They will give any fintech startup a run for their money!

On the lending front, ICICI Bank has partnered with Fintechs- FlexMoney and ShopSe to offer instant cardless EMI facility at 2500+ merchants. They have also partnered with gold loan name Rupeek as a banking partner, and recently as a strategic partner in Faircent to create P2P lending opportunity through ICICI Securities

ICICI Bank has tied up with Niyo, a neobank, to issue prepaid cards for MSME workers. MSMEs can get ‘ICICI Bank Niyo Bharat Payroll Card’ powered by Visa, for their blue-collar workers. ICICI Bank also has an initiative, wherein it allows secure and seamless integration of its core banking functions with Fintech startup InstantPay’s Neo Banking Platform to offer next-gen banking services.

In terms of payments, ICICI Bank has partnered with Visa to drive the 'Visa in a Box' program to accelerate fintech enablement for innovations across digital issuance, lending and prepaid use cases. The bank also has a partnership with Amazon Pay, where it offers a co-branded card, which has on boarded over 2mn users.

ICICI Bank has also partnered with a couple of Fintechs in the security space such as Bitgram- which uses a blockchain base to ensure data integrity and risk monitoring platform SLO technologies- where it has bought 7% stake as well.

Following lists down all fintech partnerships for ICICI Bank -

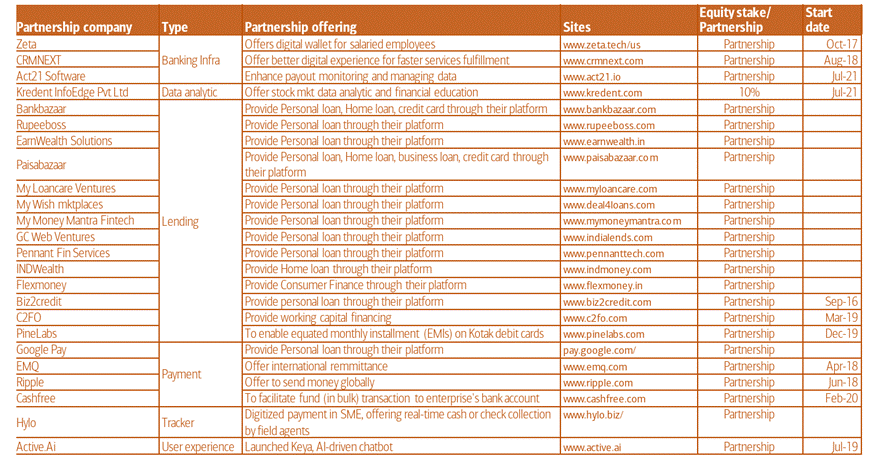

Kotak Bank

If there’s one bank that has gone big on lending partnerships, it’s Kotak.

Kotak has the largest number of partnerships in the lending space. Most of these partnerships are for sourcing of loans. Amongst their partnerships, most are on the personal loan front with names like GooglePay, Pennant Finance amongst others. They also have many partnerships on the personal finance space such as with Amazon and Flexmoney, on the home loan front they have a partnership with INDWealth and with names like Paisabazaar and Bankbazaar they have partnerships across a wide range of loan products.

Kotak has entered into partnerships with Fintechs like Zeta which provides a digital wallet for salaried employees. Under the partnership, Zeta offers 10 digital tax benefit solutions to the bank's customers that have salary accounts and they also receive a Zeta-Kotak co-branded card that can be used for employee benefit payments. The partnership with CRMNEXT has enabled Kotak to create digital journeys for faster fulfillment of its products and services ranging from account opening to lending.

Following lists down all fintech partnerships for Kotak Bank -

Federal Bank

It’s one of the most active banks in terms of fintech partnerships and punches above it’s weight when it comes to Tech.

The bank has partnered with two Neobanks as their banking partner- Fi and Jupiter. Fi was launched, while Jupiter recently got launched- and is currently operating on an invite only model. Through these partnerships, the bank aims to acquire more customers digitally over time.

On the payment front- the bank has various partnerships- for various aspects of payments as well as instant loans through payment platforms- such as Google Pay, Airtel & Cashfree. They have partnered with PayU for EMI checkouts and with FlexMoney to provide debit card EMIs. They have also partnered with Ripple for global cross payments and with Visa to launch Visa Secure- a global authentication program.

Following lists down all fintech partnerships for Federal Bank -

There are other banks where fintechs are playing a key role and the list will only grow from here onwards.

So, what’s next in the space?

A lot of focus on acquiring customers (both assets and liabilities side) can be witnessed in the current JVs and partnerships. Apart from Banking Infra B2B arrangements, I see a lot of SaaS based firms partnering with banks and growing together. Something like an expense management software, which can be used accross corporate banking clients can become big.

There has been cases where banks have stopped partnerships, most visibly by IDFC bank. In the current scheme of things, banks have an upper hand when it comes to working with Fintech and I see that changing once regulations for Digital banking comes into play. Till then, the buck does stop at the banks.

Just distribution, which seems to be the key USP that fintechs provide, doesn’t seem to be enough. They need to have the ability to manufacture financial products (loans, insurance) and have risk capabilities, which is the missing part currently. Long way to go.

Hirings in Fintech

Dice is looking to hire for multiple roles, including growth head, partnerships and more. Reach out to me and will connect with the right person.

Paytail is looking to hire for multiple positions, including growth and B2B marketing. Please reach out to me and will connect with the founders.

Xpresslane is looking to hire a Sales and Marketing Head. Super interesting role with good equity on offer. Reach out to me on abhishek@indiafintech.in and will connect with the founders.

Nimbbl is hiring for multiple positions. Reach out to co-founder, Anurag here.

M2P Fintech is hiring for multiple positions, including a product manager. Reach out to Franklin for this role.

Some of the interesting happenings in the Fintech Industry

Indian fintech Uni raises $70 million for its pay-later cards offering. General Catalyst led the one-year-old startup’s Series A funding. Eight Roads Ventures, Elevation Capital, Arbor Ventures as well as existing investors Lightspeed and Accel participated in the round.

PhonePe becomes the first player to tokenize cards on Visa, Mastercard and Rupay.

Investment-tech startup Stack has secured $4.5 million in a seed funding led by Y Combinator, Harvard Management, Goodwater Capital, Soma Capital, Uncommon Capital and Earlsfield Capital. Other investors that participated in the round include Magic Fund, Side Door Ventures, Dragon Capital, Emles Ventures, Grand Park Ventures, Chandaria Capital, Cleo Capital, AngelList, West Quad, and Olive Tree Capital. Stack builds tailored investment strategies with globally diversified portfolios for everyday investors according to their risk appetite and goals.

Top Fintech news across the world

Tiger Global backs fintech CreditBook in first Pakistan investment

The Argentinian Chamber of Fintech, a membership-based organization whose goal is to lead the digitization and modernization of the financial services industry, issued a series of recommendations for the upcoming regulation of virtual assets in the country.