Credit cards on UPI – A gamechanger for good or something to be wary of? Episode #32

Credit cards on UPI – A gamechanger for good or something to be wary of? Episode #32

Too much excitement, too many uncertainties to be ironed out. Great potential though.

Welcome to the 32nd episode of Indiafintech. It was a long time coming. It also coincides with Kissht raising $80mn, a news which reinforces my belief that there is a lot to do in the lending space – mostly offline. There will be players who will become huge here, with both scale and risk controls. More on this later on.

Today, I am gonna dive deep in to something which has been the key talking point across every conversation that I have had during the last two days – What does RBI allowing RuPay credit card really mean for the ecosystem and will it lead to increase in number of credit cards in India, due to a large, robust network of QR codes based UPI accepting merchants in the country. Sample this - 2021-22, there was a total of Rs 16.83 lakh crore worth of UPI person-to-merchant transactions, as against Rs 7.3 lakh crore worth of debit card transactions and Rs 9.72 lakh crore worth of credit card transactions, according to RBI data. UPI processes a mammoth 10x in person to person transactions monthly that it does on person to merchant, but then, this data is not that relevant for our discussion here.

Overall, what it looks like is that the evolution of the Unified Payments Interface has entered its next chapter with the Reserve Bank of India permitting banks to link credit cards to the payments platform.

But then, are we cheering too early? What are the key considerations here? Let’s dive in.

Note – In case you are a fintech founder, looking to raise funds, I might be able to help. Reach out to abhishek@indiafintech.in. In case you are looking to invest in Indian Fintech, reach out. Would be happy to help.

What do we know about credit card acceptance on UPI till now?

From the RBI’s Statement on Developmental and Regulatory Policies yesterday:

In order to further deepen the reach and usage, it is proposed to allow linking of credit cards to UPI. To start with Rupay credit cards will be enabled with this facility. This arrangement is expected to provide more avenues and convenience to the customers in making payments through UPI platform. This facility would be available after the required system development is complete. Necessary instructions will be issued to NPCI separately.

As per the guideline issued, RBI has allowed linking of credit cards to UPI. It is an interesting development as it opens a channel, which has been successful for making payments. This would begin for Rupay-based credit cards but eventually we have seen the regulator preferring an interoperable platform once the initial challenges are addressed. General sense in the industry and founders is that all other card networks, such as VISA, Mastercard, Amex and Diners will be allowed to join in pretty soon.

How easy is the transition going to be for the merchants here?

I am not too sure of the changes to regulations from the network provider (Rupay). The merchant has to be made aware that there is a possibility of charges (MDR) that could be deducted when a credit card is used on an UPI QR code. The ‘no-charge on UPI’ has been a key reason for the success of the acceptance of UPI as a payment product from consumers and merchants. And having two different flows for credit cards and other instruments, will take away one thing which has contributed hugely to UPIs success – It’s simplicity.

As per my understanding, a traditional network requires the merchant to agree to both debit and credit transactions but in UPI, the merchant has accepted UPI-based transactions. There are few options here from the initial reading:

a fresh agreement with all the merchants (181 mn UPI QR codes as of April 2022) through the network provider, which implies that there could be pushback if the flow moves more towards credit over traditional UPI,

have different formats of UPI where credit card may/may not be accepted so that the merchant is free from the worry of MDR charges. Note that we already have Bharat QR codes, which accept all formats of payments but utilization is low,

changes to MDR (Rupay credit card MDR is similar to other providers, albeit at a lower rate) by the network provider with discussion with card issuers/acceptors. At this point, NPCI could solve this challenge if there is a pushback from either party.

However, if it tilts towards the merchant (closer to zero MDR), then it would imply card issuers probably pushing back issuances of Rupay-based credit cards in the short term. We have already seen most of the private sector banks being reluctant to issue Rupay Debit and Credit cards due to MDR issues.

Which brings me to the most important missing piece – Who pays the MDR and who pays for the lending costs?

At this point the central bank has only introduced the arrangement for UPI and credit cards. Pricing of transaction or interchange fees will be decided in due course, RBI deputy governor T. Rabi Shankar said during interactions with the media yesterday.

“The basic objective of linking credit cards to UPI is to provide a customer a wider choice of payments. Currently, UPI is linked to debit cards, savings accounts or current accounts. But how the pricing of that will work out, we will have to see because pricing is something that the banks have to do,” he said.

MDR, is a fee charged by banks to merchants for processing payments. This fee is usually split between the acquiring bank (the bank whose card machine a merchant uses), the card network (such as Visa or Mastercard) and the issuing bank (who issued the customer or payer’s card).

The question of caps and rules on MDR have been a central point in electronic payments for some years now and a hotly debated one. The RBI, for instance, in December 2017 limited the MDR charged to merchants for debit card payments at 0.4-0.9% (depending on the transaction size). Similarly, the government in January 2020 mandated that merchants should pay no fees for accepting UPI payments; this zero MDR policy applied to RuPay debit cards as well, while on RuPay credit cards banks can charge merchants 0.4-0.9%.

On credit cards from all other networks, however, there is no cap on the MDR charged, and it can vary from 1.5% to 3%, depending on the bank, the card variant and the rates a merchant is able to negotiate. Effectively, this means that the MDR on Visa and Mastercard debit or credit cards is higher than that on the indigenous platforms UPI and RuPay. And that’s how one gets all those nice reward points, free lounge access and free hotel stays on some of the credit cards. Someone gotta pay for this – and that someone is usually the merchant.

Coming back to UPI, since UPI payments have no MDR, but RuPay credit cards do, what happens when someone pays at a store with a RuPay card linked to UPI?

Also, Under UPI 2.0, which allows UPI transactions for overdrafts, the MDR is 2% so there is a construct and precedent. So this is not an insurmountable problem, but the bigger question is how the security and risk guidelines work here.

The open question that remains is what happens to the MDR and the revenue-side of things. Ideally, it should be in line with the market and maybe NPCI will decide the final rate. But I am hearing that there could be a subsidized rate for some time to encourage adoption.

The big question is what the MDR will be on UPI plus credit cards. If it is made zero just like on normal UPI transactions, then there is no incentive for banks and payment gateways but only convenience for the customer. If the MDR is zero, then ideally it should be reimbursed by the government.

Ahem…

Another concern is how an MDR or transaction fee would be communicated to small merchants. The success of UPI was in that all a merchant needed was a QR code sticker and that payment processors wouldn’t take a cut of every transaction.

The merchant is used to zero MDR on UPI, so do they understand that UPI plus credit card has a higher MDR?, is a key question. The concern here is not on the credit card swipes on e-commerce as they will bear the MDR no matter what it is, but for smaller merchants. Industry players need to figure out how to explain to them that such transactions would attract a MDR compared to normal UPI transactions. They need to deliberate as an industry on how to launch the feature, whether it will be restricted and other aspects

And here comes something which I have been thinking since the news broke – Could it be a way to introduce MDR on ALL payments, including UPI, RuPay Debit card and thus, is it THE monetization moment for all fintechs which scaled rapidly due to the ubiquitous QR codes, but struggled to generate revenues? Interesting times ahead, in multiple ways.

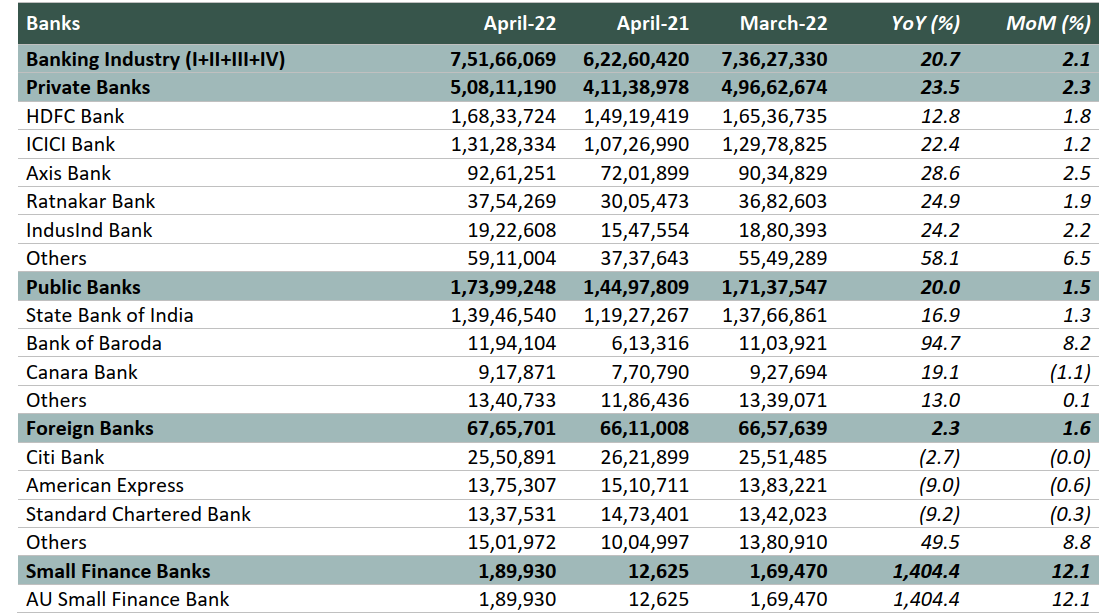

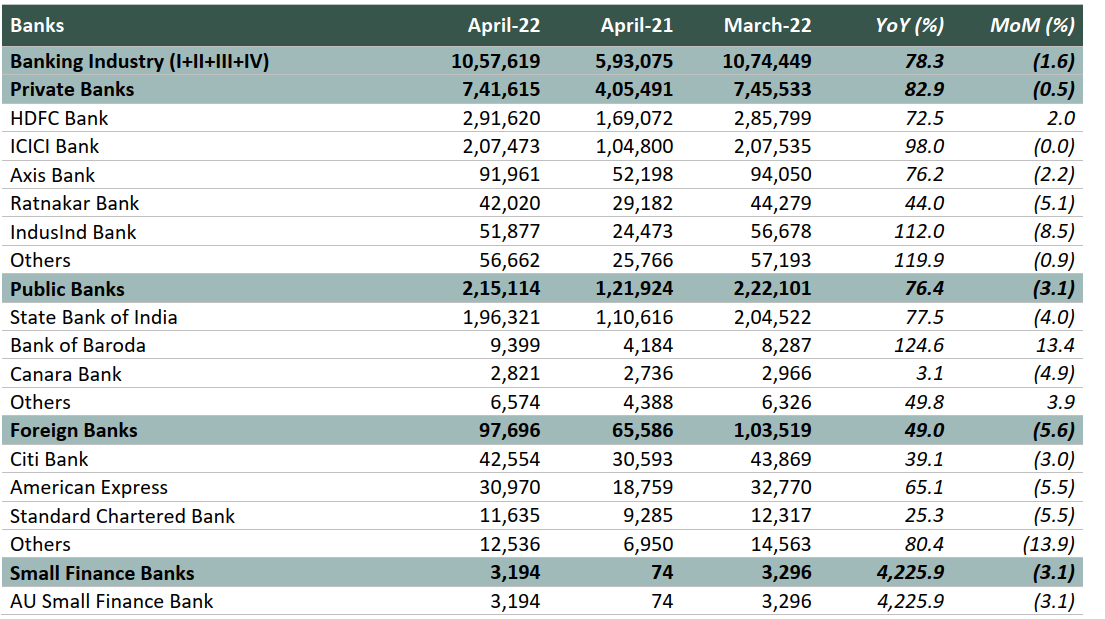

But what about the core product – Credit cards? What’s the market like? How has it been growing?

There is a fundamental question here which is not being asked enough – Is the credit card’s low penetration a result of lower demand or is it a supply problem? There are ~7.5 Cr total credit cards in India as per RBI’s latest data (May’22).

However, there are only around ~3.4 Cr unique people carrying any credit card – Penetration has remained really low despite some strong growth in the industry. Overall, industry grew by a whopping 78.3% in terms of credit card spendings in Apr-22, compared to Apr-21 and it grew by 20.7% in terms of increase in overall credit cards. Which basically means people are spending more and more on credit cards – the question is, is it increased usage due to convenience or is it because of the economic situation.

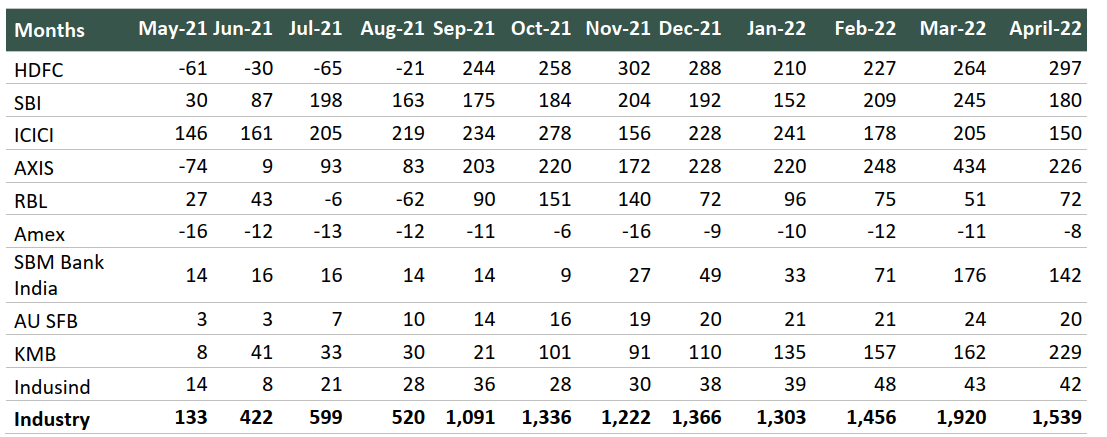

In terms of new cards issued, HDFC and Axis bank has been leading the pack. Amex has been bleeding due to the RBI imposed restriction and is the only card network which is yet to complete the data localization needs.

Number of new cards issued (in 000s)

So, what does the future hold now?

I strongly believe that the enthusiasm around credit card spendings on UPI is misplaced, for now. Cumulative new cards being issued monthly is at ~15Lakhs monthly and this is also now stagnated/in downtrend. There needs to be renewed focus on truly inclusive solutions with cards for lower income segment population, something which most banks have avoided till now. Realistically, all banks end up chasing the same top ~3-3.5 cr customers for their credit card offerings and this needs to undergo massive change for UPI+Credit cards to become a hit.

Another key issue is the uncertainty regarding MDR. It needs a clear solution. Merchant education and onboarding is another issue. Overall, loads of specifics need to be ironed out before this becomes a hit. Has the potential, nonetheless.

That’s it from my side today. Do reach out to abhishek@indiafintech.in in case you want to discuss anything on fintech. Happy to do so.

Some recent happenings in the fintech industry

After a lot of layoffs and firms downsizing, this week has seen some resurgence of funding news. Looks like things are getting back on track, slowly, but surely.

Consumer lending fintech firm Kissht has raised $80 million as part of a fresh funding round led by Vertex Growth and Brunei Investment Agency.

Re-commerce platform Cashify has raised around $50 million in its Series E round led by Prosus. The Gurugram-based company had raised $15 million in Series D funding round in March last year.

MSME-focused fintech lending platform FlexiLoans.com on Tuesday announced that it has attracted nearly USD 90 million in Series B funding from marquee investors including Denmark based PE firm MAJ Invest, UK based fintech investor Fasanara Capital and the family offices of Dr. Harry Banga and Yogesh Mahansaria.