Episode 21 – Deep dive into One click checkout products

Episode 21 – Deep dive into One click checkout products

Checkout dropouts are crazy high. Very few people are solving for this. This is set to explode.

While talking to Ashwin, founder of Xpresslane, something interesting came up – almost 70-75% e-commerce shoppers leave their shopping cart at the checkout stage! It’s probably one of the least thought for and solved for touch point, despite it being the largest problem that reduces revenues of every e-tailer by an estimated 40-45%. The drop offs for checkouts on mobile is even higher - ~85%.

What’s interesting is that billions of dollars are spent on advertising, product/UX/UI design to bring customers to website and then incentivize them to add to cart, but almost zero thoughts on how to prevent people from dropping out once the hard work has been done!

Enter the like of BOLT, FAST in US and Xpresslane, Nimbbl, Gokwik in India. They are yet to become mainstream, but I see them as a percussor to embedded finance plays in India, like Paypal or Adyen does in the west. Even Visa/Mastercard has been toying with the idea of one-click checkout products via acquisitions.

Note – In case you are a fintech founder, looking to raise funds, I might be able to help. Reach out to abhishek@indiafintech.in. In case you are looking to invest in Indian Fintech, reach out. Would be happy to help.

So, what exactly is the problem?

Twenty five years ago, there were no tools for selling online. Doing so required building infrastructure from the ground up. Most early commerce players tried but struggled with this daunting technical challenge on top of changing nascent consumer behavior.

In 1995, Amazon was born with Amazon Marketplace coming shortly thereafter. Sellers flooded the platform because it provided end-to-end commerce infrastructure and consumer distribution. Consumers had one destination to go to for buying things online with low prices, quick shipping, and a single click checkout experience.

A win-win situation, right? Not exactly. Online sellers began to realize whatever traction they had would quickly disappear. Selling on Amazon meant fierce competition, zero brand loyalty, and no direct relationship with customers. If sellers made too much money, another seller, or even Amazon itself, would find a way to produce the same product at a lower cost. To build a big business, it was abundantly clear that sellers needed their own customer relationships.

Enter the shopping cart or what we call the D2C revolution: website building software that enabled add-to-cart functionality – Say, Shopify!. This became the core commerce platform with 100+ different players surfacing between 2000 and 2010. As a result, carts evolved from simple website builders to the core integration hubs for ecommerce enablement tools. As the integrations piled up (sometimes 100s or 1000s per cart), so did the carts’ fragility; they were never designed to handle massive scale middleware and the complexity behind the entire checkout process. This ultimately created incredible frustration for merchants managing the intricacies of a checkout stack on their own.

Now the problem part - Shopping carts are expected to do everything… but everything is a lot. What it takes to power a full ecommerce store is very complex.

The checkout experience starts when a user decides what they want to buy and has an intent to purchase. It presents payment options to consumers, collects shopper’s personal information, processes payments, mitigates fraud and connects to dozens of backend systems that are required to power the transaction. For the checkout experience, arguably the most critical piece of ecommerce, reliability and ease-of-use are king. Checkout has to constantly be tested, updated, and leveraging the latest and greatest connected tools.

As a merchant finds product-market fit and begins to scale to millions of GMV, they begin to take notice of the fact that shopping carts don’t have checkout in their DNA. With considerable volume occurring through the site and the marginal cost for each new shopper increasing, converting users on their site becomes paramount.

Losing a customer at the final step, checkout, is tragic because the marketing rupees have already been spent to get the customer to land on the site. The customer has become interested in a product, found it in stock and in the right size/color, and clicked checkout — which means there was strong intent to purchase.

In India itself, E-com would be $120 Bn market by 2023 with Non Amazon, Non FK (NANF sites) being $40 Bn. As per various D2C companies, checkout failures itself is around worth $12-15bn yearly!

Big, big opportunity to be captured!

So, why does it happen?

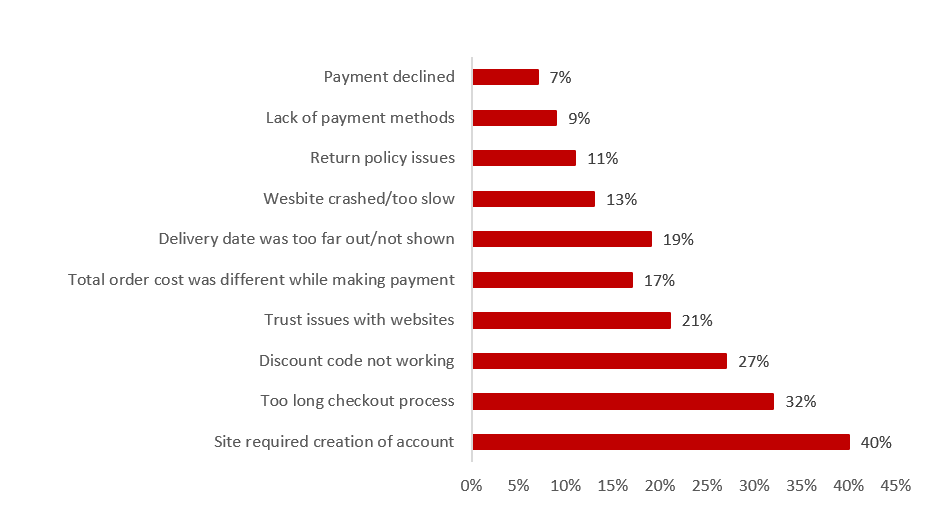

There are a multtiude of reasons, but the following captures most of it -

Source: Abhishek Kumar

The top issues are actually convenient related issues. I have, myself, left so many purchases after coming to checkout page because they were either forcing me to create an account, which in itself is a huge process or there were so many data inputs needed, that I ended up deciding to buy it from Amazon since I didn’t need to do all of this AGAIN.

Other key issues are trust issues with newer websites. Sample this, you like the product or there is a new website selling a product that no one else does, but I am wary of putting in both my login as well as financial info there. Or the very painful issue of slow websites, lack of payment methods (this is actually a very big issue, even with well established brands), multiple payment failures and so on and so forth.

So, what’s the solution?

Now imagine one product to solve it all! One, single click login across multiple e-tailers which stores your information, thus eliminating the need for account creation every-time you visit a website, with your preferred payment option stored and available across every e-tailer? Effectively, your identity is now secured at one place and is being used across multiple platforms by you. So, any platform related concerns are alleviated.

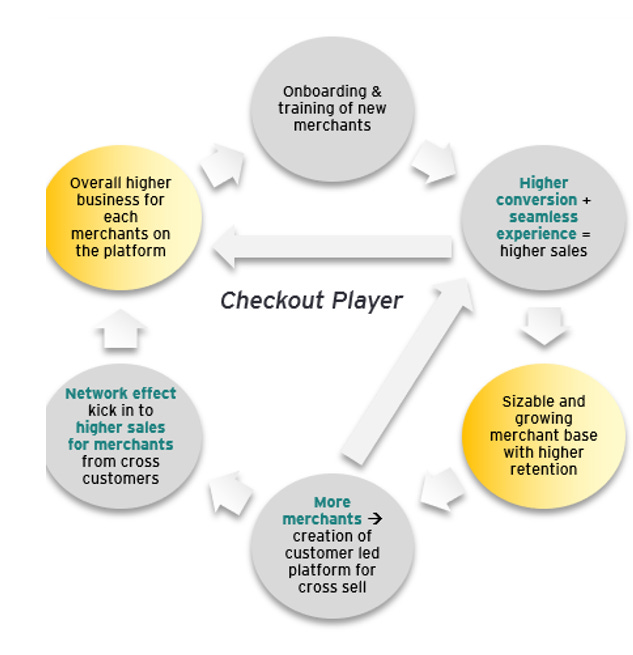

At enough scale, like what BOLT has done, this creates a very positive network effect as well. Larger number of merchants leads to higher customer on platform, incentivizing newer and larger merchants to be part of the platform and so on and so forth.

Source: Abhishek Kumar

Sample the following at BOLT –

So, in clothing , 14.5% sales are now coming in from network effect – People buying at X platforms also end up buying from Y platform since there is almost zero friction and platform discovery is super easy. So, in effect, what started as a solution to reduce purchase friction, has now turned into a high value, high intent, customer acquisition platform!

In India, there are 120+ funded D2C brands doing business on their own website and the number of brands doing it is 800+! In India, 23,000+ shopify stores were created in last 5 months alone! There is a ready market for this, in bulk!

So, who are the Indian guys solving this issue?

There are few, but I am most excited by Xpresslane, Nimbbl and Gokwik. Each solving issues in their own way.

Xpresslane looks to be the most complete solution currently.

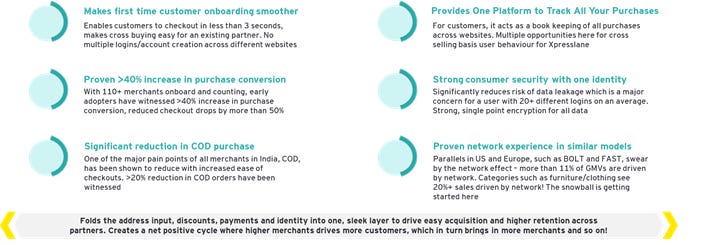

It solves one click problem for users, conversion problem for merchants and in the process, is creating an amazing, network effect led flywheel which will feed its growth.

Interestingly, it provides a very interesting dashboard for users where she can see all her purchases ACROSS platforms. I see this becoming a very powerful consumer platform, where merchants will flock to list.

Xpresslane is well poised to make a big dent in the market.

Source : Abhishek Kumar

Xpresslane is payment method agnostic as well as platform agnostic and can be easily customized to suit for other geographics, thus opening up newer growth channels.

GoKwik has been the flagbearer of the industry for some time now.

Their stated vision is to increase GMV of internet economy by democratizing shopping experience. They are doing this by focussing on UPI as a payment solution and reducing RTOs, which is a major COD problem as well as overall e-commerce problem. They also bring in fraud detection capabilities (similar to BOLT) and aims to reduce COD frauds.

Interestingly, they insure fraud orders. All orders through GoKwik Checkout are insured for RTO for a % commission on every transaction.

They just raised $5.5 mn from Matrix partners, RTP Global and other investors. They have limited themselves in payment options and RTO reduction, but there are opportunities for embedding financial services here, including working capital for their merchants and credit products for the end consumers.

Nimbbl is probably following FAST and looks to be a complete 1 click solution, very close to what Xpresslane is doing.

They recently raised $1.6mn seed round from the likes of Sequoia and others.

Nimbbl focuses on growing business with a 1-Click checkout experience, gives access to leading BNPL modes & simple pre-built integration with multiple payment gateways. These guys are probably the most advanced in terms of embedding financial solutions.

Love this on their homepage. Shows their thought process in terms of the network they are creating.

Interestingly, they also provide a dashboard to manage payment preferences. Here’s what they say - Manage priority of the Payment Gateway Providers and track their fees, enable or disable a payment mode, run offers or discounts and run your entire payment operations from one dashboard.

This is actually pretty interesting. Combined with purchase tracker, this gives very interesting view to the consumer and has the potential to be a great platform for customer acquisitions.

There are other Indian firms doing part of the solution such as GoSwift.

Feels like investment in this particular area is underdeveloped and there is a lot to be done, both from founders side as well as from the investors side.

Global experiences are amazing here!

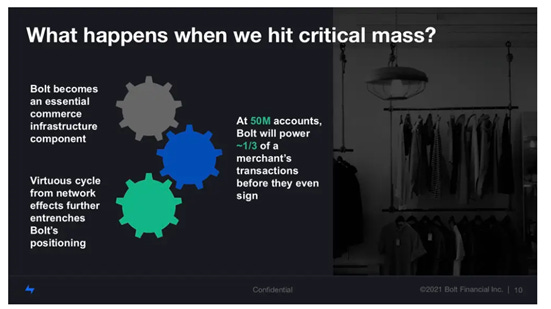

BOLT, which provides 1 click checkout solution combined with fraud detection recently entered Europe and raised $393 million from a host of investor. Love the way they presented the below!

FAST, which just raised $100mn from the likes of Stripe and others, is an end to end solution for checkout. They are trying to create a consumer led solution, which will turn into an acquisition platform sooner than later for merchants.

So, what’s next?

I see similar growth happening here in India! A great story to track! All the growth drivers are in place and this is a D2C growth story, combined with opportunities for embedded finance (Nimbbl already doing this).

This is the next frontier in the consumer -finance-tech grouping and I see a lot of interest in the space.

That’s it from my side on this episode. Feel free to reach out to me in case you want to connect with founders in the space. For collaboration or investing.

Hirings in Fintech

Nimbbl is hiring for multiple positions. Reach out to co-founder, Anurag here.

M2P Fintech is hiring for multiple positions, including a product manager. Reach out to Franklin for this role.

Xpresslane is looking to hire a Sales and Marketing Head. Super interesting role with good equity on offer. Reach out to me on Abhishek@indiafintech.in and I will connect with the founders.

Antrepriz is looking to hire for multiple roles, including growth head, partnerships and more. Reach out to me and will connect with the right person.

Finovate is looking for program managers in CEO’s office. Do reach out if you are interested

Kudos is hiring for a business analyst and a graphic designer. Reach out to either me or the founder, Pavitra here.

Some of the interesting happenings in the Fintech Industry

Bengaluru-based fintech startup Neokred Technologies Pvt Ltd said it has acquihired a buy-now-pay-later (BNPL) solutions provider PeSeva Technologies.

Non-banking finance company (NBFC) Five Star Business Finance (FSBFL) has filed it’s DRHP with SEBI. According to the DRHP, the company will raise up to Rs 2,751.95 crore via a primary stake sale. The issue will entirely be an offer-for-sale (OFS), where its promoters and existing shareholders will offload stake.

PayTM is seeing some interesting times. Institutional investors have subscribed 0.24x on close and interestingly, GMP has crashed from Rs.155 to Rs.40. What does this mean now?

Stratzy, an investment advisory platform, has raised $800,000 in a pre-seed funding round from Leo Capital, Titan Capital, and First Cheque. The platform has more than 10,000 users and expects to clock one million downloads by 2022.

Amazon Pay (India) Private Limited, the digital payments arm of the e-commerce firm, reported its revenues for the financial year 2020-21 as Rs 1,769 crore. This is a 29 per cent jump since the last financial year.

Open, which just raised $100 million from Temasek, Google, Visa International and SBI Investment, with existing investors Tiger Global and 3one4 Capital also participating claimed they have done transactions worth over $20bn.

I am happy to get on a call and discuss any fintech related topic or take feedbacks, suggestions. Do reach out!

Good read, thanks for this post !!