Episode 23 – BNPL is becoming widespread, globally and in India. It’s now one of the biggest enabler of e-commerce

Episode 23 – BNPL is becoming widespread, globally and in India. It’s now one of the biggest enabler of e-commerce

Globally, BNPL is becoming a serious challenge for Credit card firms. See a different trajectory for the same in India.

One of the most interesting news this week was Amazon actively removing Visa cards as one of their key card players in UK. Amazon is offering 20 pounds off a purchase, to customers who primarily use Visa cards as an incentive to update payment method. Affirm is supposed to be the biggest beneficiary of this! More on this later.

In India, BNPL players are already witnessing decent traction in the current festive season across e-commerce platforms. Flipkart and Amazon, which provide ‘pay later’ options, have seen a spike in BNPL usage amid their annual festival season sales. During the Great Indian Festival 2021, the usage of Amazon Pay Later surged ~10 times. Flipkart’s Pay Later accounted for the second-highest share of payments after paid orders, even higher than the Unified Payments Interface (UPI) as a preferred mode of payment.

Overall, it looks like BNPL is becoming more and more mainstream and taking share from Credit Card providers worldwide. In India, it’s providing credit to people at key decision touchpoints, both online and offline. A good chunk of these people didn’t have this access to credit till now.

Note – In case you are a fintech founder, looking to raise funds, I might be able to help. Reach out to abhishek@indiafintech.in. In case you are looking to invest in Indian Fintech, reach out. Would be happy to help.

BNPL in India – Where does it stand today?

Buy now, pay later (BNPL) is a short-term financing service that allows customers to spread out their payments (from 30 days up to 12 months) for a purchase, usually without any additional interest. In India, local kirana stores followed the khata system for regular customers, where the store owner would keep accounts of daily purchases and seek payment later. This BNPL system is not very different, except that the khata has now moved online.

BNPL is making promising progress (USD3–3.5bn disbursals in FY21), and is being seen as a secular trend and not just a flash in the pan. Underlying reasons for the same are i) largest addressable market (huge mid-income, demographic dividend etc), ii) proliferation of e-commerce, with expected consumer internet market of USD200bn by FY26, iii) changing financial behavior–consumption oriented mindset; and iv) lower retail credit penetration form a perfect cocktail driving uptake of BNPLs.

How does BNPL work?

Usually, BNPL loans are offered via tie-ups among retail marketplaces, merchants and financiers. As there is no interest rate, the facility is offered to customers with a merchant discount rate – or a transaction service rate – of around 1.5%. In some cases, a subvention rate regime is implemented where a part of the interest rate is borne by the merchant or the fintech platform. For a discussion on BNPL models in India and their unit economics, please visit my earlier post here.

From what I have observed, most BNPLs are burning cash currently as typical margins are quite thin, which are more than offset by discounts. Direct discounts and cashback promotions are widely rolled out to beat stiff competition among top players. Transaction volumes have increased as a result of this, but the contribution margin is still negative for all the top players.

While there has been enough stories around players such as ZestMoney, Simpl and other similar players focused on online e-commerce, there are some interesting players tapping the larger, much lesser under-penetrated offline market. Paytail is one such interesting firm and I believe this particular segment will get interesting for investors soon enough.

What is driving the growth in BNPL offerings?

It’s a combination of ease of access to credit for customers (Convenience + Credit) for customers, higher conversions at higher AOVs for merchants (multiple reports say AOVs shoot up by up-to 45% when customers are provided with instant pay later options at checkout. The number is higher for offline merchants than online merchants!) and a much larger market for the lenders. Effectively, it’s a three sided flywheel that feeds into itself.

BNPL seems to be a win-win for all stakeholders with creation across value. This is one of the main reasons for the product’s speedy uptake.

Certain global markets showcase significant success stories

Internationally, there has been significant proliferation of BNPL players, of which few have scaled up significantly and with global addressable market size estimated at USD22tn (source: JPM), there are expectations of sustained growth.

Consequently, internationally the market is beginning to heat up with Square buying out Afterpay in a USD29bn deal, PayPal buying Paidy (Japanese) in USD2.7bn, creating a buzz that Affirm, Klarna, Sezzle, and Zip could also go under. Moreover, news that Amazon, Walmart and Apple are all looking to jump onto BNPL bandwagon has created a halo around the BNPL business model.

Globally, Sweden, Germany, Australia and few others have seen deep BNPL penetration in a very short time, despite high credit card penetration.

India is seeing promising trend, but key differences may restrict similar scalability

BNPL is emerging in India with the presence of several fintech platforms - In addition to pure-play BNPL start-ups such as Simpl, Lazypay, Zestmoney, ePayLater, and e-commerce marketplaces such as Flipkart and Amazon, Indian fintechs also offers their own BNPL products. Older payments companies such as PhonePe (via Flipkart) and Paytm have also ventured into this territory.

Not only this, India’s biggest banks are already testing this arena – HDFC Bank’s “FlexiPay” and ICICI Bank’s “PayLater” among others.

That said, there are certain key differences in the Indian context: i) basic working model is different – sales facilitator versus payment options in India; ii) challenges in customer acquisition & merchant monetisation; and iii) very nascent market, which positions India differently.

Different business model at play: One of key differences in global and Indian context is the inherent difference in underlying business models. Players with scale in international market have morphed into sales facilitators from being a payment option (as is the case in India).

Interestingly, leading BNPL providers have built integrated shopping platforms that engage consumers through the entire purchase journey, i.e. from pre-purchase to post-purchase. Affirm, Klarna are now seen as a major customer acquisition channel and not just credit providers. While in India, they are solely seen as payment and pure financial offerings. Simpl has been trying to move in the marketing direction, but long way to go.

Challenges in acquisition and merchant monetisation: One of the key differentiators in global-scale BNPL players and those in India is the ability to acquire merchants and simultaneously monetise them.

For international peers, >70% of revenue comes from merchants (take rates are higher at 4–6%), however, in Indian context the ability to charge merchants is much lower given proliferation of payment platforms riding UPI (a non-monetisable public digital architecture). This poses a revenue problem for most Indian players.

Nascent market: BNPL in Indian context is a very recent phenomenon, and the entire value chain from lenders, merchants, consumers and technology providers will take time to mature.

Also, looking at scaled-up businesses such as Klarna, Affrim and AfterPay, it took all of them (around a decade) to graduate and build acceptability. One of the key aspects is customer graduation/ credit culture development. That journey in India will take time to play out.

Overall, there are certain variables that need to be monitored from Indian perspectives here –

Customer fees: Globally there has been a lot of concerns on higher customer late fees/interest rates that BNPLs charge. This trend has been reducing, with customer fees coming off gradually (across major larger players—although not a pervasive trend still). Expect a similar dynamic to play out in India over time , but the problem magnifies given non-monetisable nature of merchants, which, cumulatively, will put pressure on revenue.

Younger population have been show to default more: In one of the surveys by a broker, 21% of BNPL customers missed payments in FY19. In fact, most completed transactions were made by consumers under the age of 35, and for completed transactions that had missed payment fees, the same age cohort accounted for 67% of these transactions.

All of this implies that missed payment is more prevalent in younger population and thus will have a higher cost attached to them. A problem in the Indian context.

Over-indebtedness leading to financial difficulties: This is a key risk that needs to be managed well is over-indebtedness caused by BNPLs. One of the recent survey) suggests: i) 20% of consumers cut back on or went without essentials (e.g. meals); and ii) 15% said they had taken out an additional loan.

These trends (more prevalent among consumers using multiple BNPL offerings) indicates serious consequences of over-indebtedness arising out of BNPL offerings. This over-indebtedness also seemingly pulls along other credit options—a similar survey finds that a consistently higher proportion of BNPL credit card users incurred interest charges on their credit cards (between 66% and 73%). While, in the same period, only 42% to 46% of other credit card users incurred an interest charge on their credit card.

Moreover, the same survey revealed that between 38% and 43% of BNPL credit card users used up > 90% of their allocated credit limit on their credit cards versus only 16% to 18% for other credit card users – indicating higher propensity for lapping up leverage.

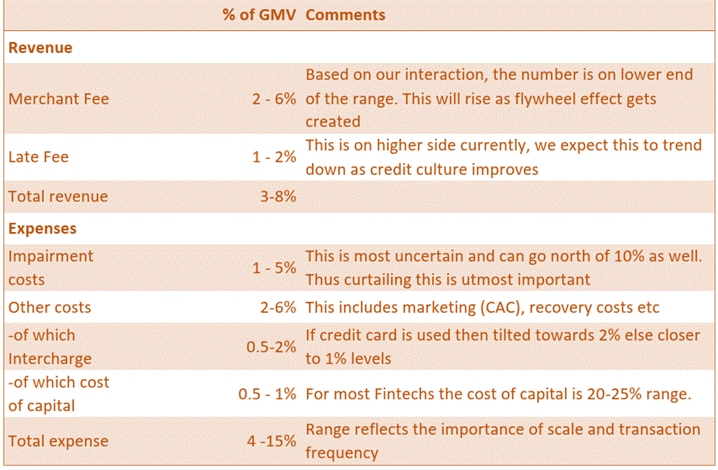

Revenue model – Largely contingent on fee income

The revenue model for BNPL is contingent on the business model, viz., customer-centric (no charge to customers) or merchant-centric (bundled with other product offerings). Consequently, revenue levers for BNPL providers are: i) merchant fees take rates from merchants (depending on GMV, generally ranging from 2–6%) and subvention income; or ii) fees from customers (late fee, monthly fee, interest rates, subscription fee). The revenue model only works when the integration between the customer and merchant exists, i.e flywheel effect does get created.

Throwing in the costs incurred by these, the profitability looks like below –

So overall, while global success is heartening, there are certain specific challenges to the Indian model which might limit the growth of the BNPL model, more so in the online play where costs are similar globally, but revenues are on the lower side here.

Also, since the credit card penetration is on the lower level, the incentives to take the market share away from these players are lower. Effectively, BNPL in India is a parallel industry, focused more on credit access than convenience and this limits the profit making abilities of players. Combined with large penetration of zero charges payment methods like UPI, the proposition to make money from merchants as well as customers by charging fees becomes even more difficult.

However, one interesting thing that a lot of players seem to miss out on is the large potential in the millions of offline stores in India.

Offline BNPL needs a revamp, Bajaj Finance has focused on larger format stores

In Mom & Pop Stores, which drive 85% of India’s retail, it is hard to get EMIs outside of Mobiles & appliances segments. There’s no easy, digital way exist for the ‘offline’ merchants to offer, & consumers to get an EMI.

Paytail has come up with an innovative solution here – they enable merchants to allow credit limits upto Rs.2 Lakhs (ticket size from Rs.3,000 to Rs.2,00,000) across both brand and non-branded EMIs. Their realtime decision engine is something super interesting – it enables quick loans via multiple API calls and prevents frauds, which is one of a kind.

Source: Paytail

Combined with very high network effects possible, this can quickly scale up to be one of the most scalable business model in Indian BNPL ecosystem. I, for one, would follow this closely.

Now, what’s Amazon doing that’s interesting for the sector?

Earlier this week, Amazon announced that it would stop accepting Visa credit cards issued in the U.K. due to high interchange fees on transactions. The company gave a deadline of January 19 and is offering consumers who primarily use Visa cards £20 off a purchase as an incentive to update their preferred payment method.

The move followed similar efforts by Amazon to curtail the use of Visa-issued credit cards in Singapore and Australia, markets where the e-commerce giant introduced a 0.5% surcharge on transactions made with those cards. In both cases, Amazon also offered customers gift cards to encourage them to switch payment methods.

While Amazon is asserting its market dominance in an effort to lower transaction fees — which a company spokesperson said “[continue] to be an obstacle for businesses striving to provide the best prices for customers” — it is hardly alone in its desire to ween customers off high-cost payment methods.

For merchants, the introduction of “buy now, pay later” (BNPL) payment options, the rise of digital wallets and a broader push toward ACH or account-to-account (A2A) transactions are all part of a strategy to reduce consumers’ overreliance on credit cards.

So, what’s next for the sector?

I do see something similar to what Amazon is doing in UK happening in India, but more so on the offline retail. Card acceptance is on the lower side anyway and UPI payments have made it easier to pay at one go without any charges for transactions. However, there is a white space in EMI based/pay later solution and it’s a big, fat white space in the offline world.

Going by the amazing UPI led payment model’s adoption here, BNPL would be lapped up, more so the 3 months zero cost types by the masses. There is a clear case for scale. However, profit models are still somewhat uncertain and this is something to closely follow and track. I do see many more like Paytail coming up, sooner rather than later. Also see the likes of Zest making inroads in the offline retail space.

Overall, we’re likely to see more BNPL partnerships and adoption as retailers seek to grow their top-line sales, reach new customers and move beyond credit cards/pay at one go as a primary payment method.

Exciting times ahead!

Hirings in Fintech

Paytail is looking to hire for multiple positions, including growth and B2B marketing. Please reach out to me and will connect with the founders.

Nimbbl is hiring for multiple positions. Reach out to co-founder, Anurag here.

M2P Fintech is hiring for multiple positions, including a product manager. Reach out to Franklin for this role.

Xpresslane is looking to hire a Sales and Marketing Head. Super interesting role with good equity on offer. Reach out to me on Abhishek@indiafintech.in and I will connect with the founders.

Antrepriz is looking to hire for multiple roles, including growth head, partnerships and more. Reach out to me and will connect with the right person.

Kudos is hiring for a business analyst and a graphic designer. Reach out to either me or the founder, Pavitra here.

Top read for the week

RBI released their much awaited working group report on digital lending, can be accessed here. One of the key recommendations - a separate legislation to prevent illegal digital lending activities. Some of the key recommendations are -

Development of certain baseline technology standards and compliance with those standards as a pre-condition for offering digital lending solutions.

Disbursement of loans directly into the bank accounts of borrowers; disbursement and servicing of loans only through bank accounts of the digital lenders.

Data collection with prior and explicit consent of borrowers with verifiable audit trails.

Each digital lender to provide a key fact statement in a standardised format including the Annual Percentage Rate.

Standardised code of conduct for recovery to be framed by the proposed SRO in consultation with RBI.

Some of the interesting happenings in the Fintech Industry

Amazon now wants to remove Visa powered cards issued in UK. Affirm probably will be the biggest gainer here.

Kunal Shah-led fintech platform CRED is in talks to acquire two startups - Dineout and Wint Wealth, as it seeks to offer more services to its over 7.5 million users.