India – A story of contradictions and possibilities, Fintech the flag bearer of startups world | #Episode 31

India – A story of contradictions and possibilities, Fintech the flag bearer of startups world | #Episode 31

India is full of opportunities. Everyone needs to expand where they are looking at.

The last few weeks have been super interesting in terms of fund raises as well as investor/founders conversations. While there was a dull period in mid parts of February, March more than made it up.

One amazing read this week was the Indus valley report by Blume Ventures. Despite it not being focused on only fintech, the takeaways are clearly meaningful for the sector and this episode is dedicated to dissecting some of the trends across the country which are detrimental to the sector.

Hop on!

Note – In case you are a fintech founder, looking to raise funds, I might be able to help. Reach out to abhishek@indiafintech.in. In case you are looking to invest in Indian Fintech, reach out. Would be happy to help.

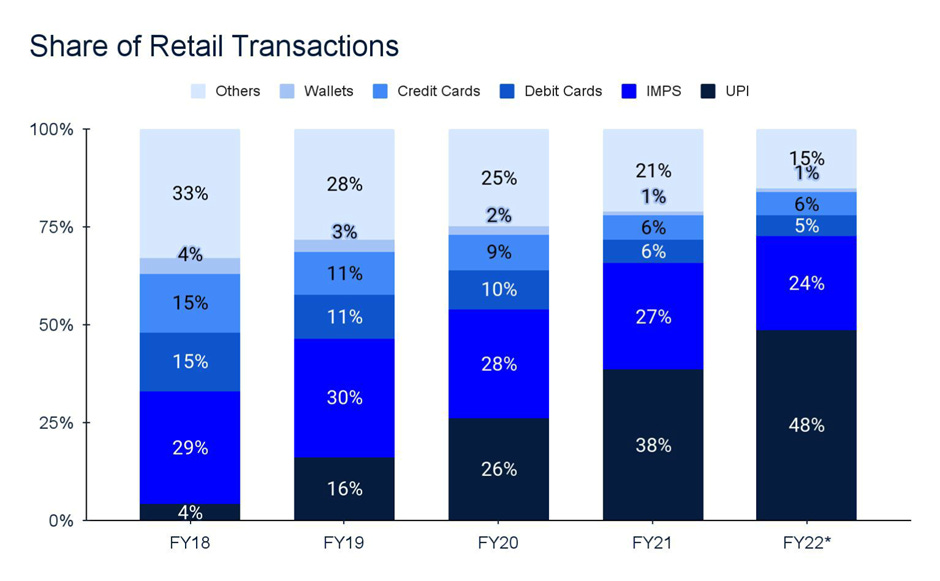

UPI/Digital payments have arrived and in style.

In less than 5 years of adoption, UPI now corners ~48% market share in all retail payments. The most impacted instrument here is credit cards – it has declined from 15% in 2018 to just 6% in 2022! And more importantly, credit cards are now facing challenges not just from UPI, but from BNPL as well. In fact, with firms like Paytail making some serious inroads in offline retail, the last frontier of credit cards also seems to be falling.

India is becoming truly digital, even in the offline world.

The interesting takeaway here is that credit card itself has been growing at ~15% CAGR, the overall low credit card penetration, stellar growth of UPI, India’s traditional comfort with credit and convenience, has left a substantial whitespace for BNPL to prosper.

I have a very bold prediction here – Number of unique credit cards in India talks about the real creditworthy and salaried people in India. However, they are missing out on people working in one of the 65 mn SME/MSMEs and are earning decent – this is where BNPL will make a serious dent. I expect BNPL firms to allow the Indian credit story to evolve without credit penetration (One of the lowest in the world at ~4%. In comparison, Canada is at 66%!) going up.

Credit cards in India will remain limited because 1) Formal, salaried jobs in India will remain limited as % of overall jobs 2) Banks don’t have the willingness to go beyond easily targetable segments in terms of salaried and formal business set 3) Customer acquisition costs for traditional credit card firms (banks) are prohibitively high and unless funded by VCs, it will remain high for NBFC led card business as well.

BNPL story is just starting in that sense. And here, I am most excited by models which are B2B2Cl focussed on merchants, which leads to negligible CACs and significantly lower NPAs. Paytail is one such firm which I am super excited about.

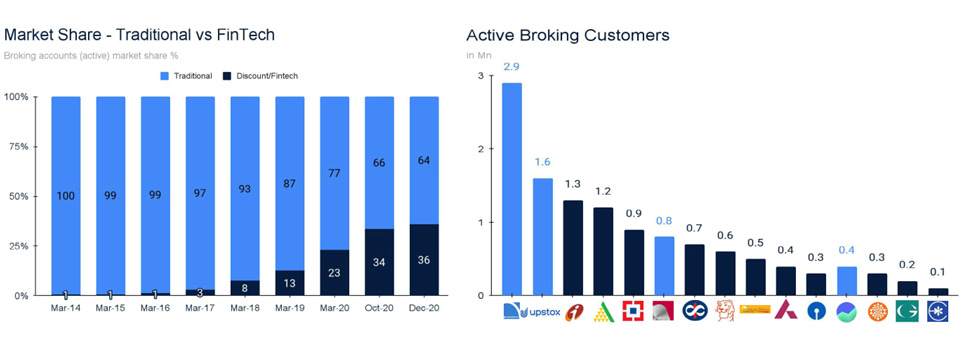

Fintech players have cracked one playbook – Building scale at super-fast speed

Fintech startups have acquired user bases and engagement in years, that have taken legacy brands decades to build. Paytm has more customers than HDFC Bank + ICICI Bank + Axis Bank + Kotak Bank + Bank of Baroda combined! Only SBI has more customers and it’s a century old, govt. led firm.

The most glaring example in scale business is the discount broking business – Zerodha has 2x customers compared to the largest legacy broker, Angel Broking as well as ICICI Bank. Upstox, a very recent startup, has more customers than each of the largest legacy brokers.

And of course, Crypto, at least going by what the industry people claim, beats all of them!

Another interesting data point – Digital lending is now 11% of retail’s loan book, which was at ~6% in 2019. The pace of growth is dazzling.

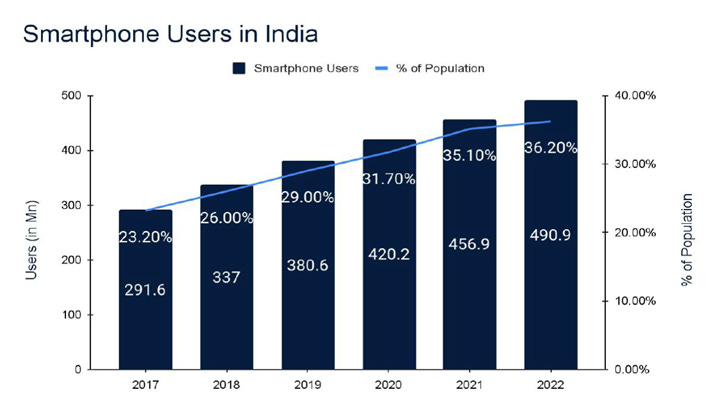

The Wang trifecta is real and I agree to it

The overall consumer economy and hence the fintech economy, takes off once three conditions are met (This was observed in China) –

· Cheap Bandwidth

· A smartphone in every pocket

· A frictionless payment system

First and third are fairly self-obvious – India is there. In terms of smartphone penetration, India has reached ~36%, as shown below and is only going to increase.

Combined all three above with a robust public infrastructure, it does seem like India infra and firms are ready to scale up.

All good till now, so what’s the roadblock!

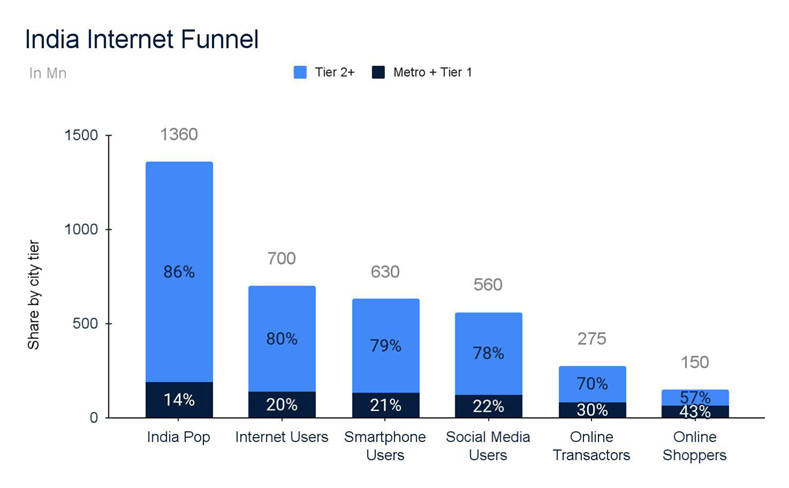

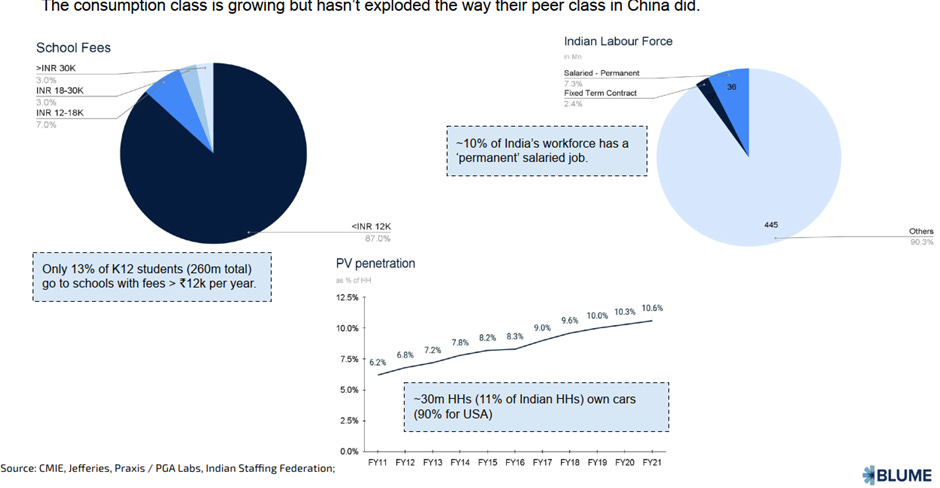

India’s consumer of services, including fintech ones, is a very small subset of the population and refuses to grow. And most startups are focusing on a very thin internet enabled consumers to sell everything. Combine this an abysmal female labor participation at 19% (Global average is at 46%) and there’s only two ways for Indian startups to grow really big – Either overall income levels rises to expand the pool or they start targeting the non-internet, offline retail economy. I would bet on the latter.

India internet funnel is narrow – Only 10% of India’s population have ever shopped online, ~150 mn people and even within this small set, 65% of these purchases are through Cash On Delivery. So in effect, only 3.5%-4% are shopping digitally – A number very, very close to credit card penetration in the country. Maybe, those banks are onto something!

There’s a bigger issue though – the real consumer class in the country with an ability to buy things is really, really small. Only 10% of the country have a permanent salaried jobs and even within this set, 65% earn less than INR 30K a month.

There’s just not enough people to buy even mass things, forget mass-premium and almost everyone is chasing these guys only! Sample this – one of the largest (by valuation) card company prides on the fact that they target only 750+ Cibil customers. It’s funny because, that’s what HDFCs and SBIs of the country are doing. But then, firms like Paytail are solving for real issues here, so there’s no lack of solution.

What it really means is that India’s fintech or for that matter, consumer problem is not tech or VC funding or problem solving problem – It’s a macro problem. India needs to increase employment and needs to increase per capita GDP as well as earnings of its population.

Unless this happens and happens at large scale, the only real models would be either B2M (P2M) or B2B2C, where merchants or brands are willing to put in money to expand the customer base.

So, what’s the takeaway?

There’s one clear takeaway – there are people with enough money who are not online. A business model which targets them, either in BNPL or any other play, will do good. Look for them.

Other is that online only fintechs are in for a rude shock – there’s not enough market for them to operate in.

Please click here to read the whole report. It’s worth the time spent.

Some of the interesting funding news in the Fintech Industry

Debt marketplace CredAvenue, which helps businesses and enterprises secure debt from lenders, has become the fastest Indian fintech startup to join the unicorn club. They raised a $137 million Series B financing round led by Insight Partners, B Capital Group and Dragoneer.

Fintech startup Credilio has raised $4 Mn in a Pre-Series A funding round from a number of investors. Led by Cornerstone Venture Partners Fund, the funding round also saw the participation of Exfinity Venture Partners and the founder of Param Capital, Mukul Agarwal as an angel investor.

Rupifi has raised $8 million venture debt led by Alteria Capital, Trifecta Capital, and Innoven Capital. This fundraise is an extension of a $25 million Series A round that Rupifi announced in January 2022.

Investment platform Groww is in talks to raise $150 million at a valuation of $4-$5 billion; it is in talks with a clutch of sovereign funds, sources said, as it continues to receive investor interest in a tepid funding environment. Its move to raise a fresh round comes six months after its $251 million Series E round, as it steps up efforts for its foray into neobanking.

Other interesting happenings in Indian Fintech

Mahila Money, Visa, and Transcorp have teamed up to launch Mahila Money Prepaid Card, a product aimed at helping women entrepreneurs use digital payments more effectively.

Software-as-a-service (SaaS) firm Perfios said it has acquired financial technology platform Karza Technologies for an undisclosed amount.

Hirings in Fintech

Paytail is looking to hire for multiple positions, including growth and B2B marketing. Please reach out to me and will connect with the founders.

Highradius, a SaaS firm for treasury, O2C and record to report is hiring for multiple roles in product, tech and sales. Please reach out to me in case you are interested.

Dice is looking to hire for multiple roles, including growth head, partnerships and more. Please reach out to me in case you are interested.

Xpresslane is looking to hire a Sales and Marketing Head. Super interesting role with good equity on offer. Reach out to me on abhishek@indiafintech.in and will connect with the founders.

Nimbbl is hiring for multiple positions. Reach out to co-founder, Anurag here.

M2P Fintech is hiring for multiple positions, including a product manager. Reach out to Franklin for this role.

PS - Do reach out for any fintech/crypto related discussion. Would be happy to get on a call and discuss.