Indian Wealthtech Landscape – Opportunities are great, who can make the most of it? | Episode #28

Indian Wealthtech Landscape – Opportunities are great, who can make the most of it? | Episode #28

New age brokers, financial management apps, debt investing are making waves.

Indian wealthtech space is lit right now! While the fact that a very minuscule portion of the population invests in the stock markets compared to other large markets is well known, what has really kickstarted the journey is a combination of easy crypto investing as well as gamification of savings and investing.

Companies such Piggy which simplifies Mutual Fund Investing and combines even the traditional EPFs to portfolios, Fello which has a super interesting Gaming interface to introduce savings and investing, Akudo, which is a learning focused Neo-bank are changing the way people see investing for good.

Note – In case you are a fintech founder, looking to raise funds, I might be able to help. Reach out to abhishek@indiafintech.in. In case you are looking to invest in Indian Fintech, reach out. Would be happy to help.

Wealthtech – An introduction

Wealthtech refers to the convergence of technology with financial assets, offering investment solutions/ tools to manage financials. With rising digital adoption and a growing base of wealthtech investors, the Indian wealthtech market is set to grow from US$23bn in FY21 to over US$63bn by 2025.

For investors, profitability has been a challenge for many platforms. Concerns are mostly around generating revenues and high cost of customer acquisition. A good number of players are moving from distributors/trading platforms to manufacturers of mutual funds. Zerodha, Upstox and Groww are among the largest wealthtech player. Some players, such as Piggy, are moving towards becoming investment management first, integrated digital bank. More on this later on.

The Opportunity - Indian market is under-penetrated

Only 2-3% of India's population invests in stocks, vs developed economies like the US, where ~55% of the population invests in stocks. The emergence of wealthtech platforms like integrated financial managers, digital brokers, bundled investing,robo-advisors etc. and emergence of new asset classes like fractional investments in lease financing/ commercial real assets is likely to accelerate growth.

Further, regulator SEBI has taken various initiatives to ensure that the sector flourishes in India- these include a regulatory sandbox for wealthtech firms to experiment on a pilot basis, allowing e-commerce entities to sell MFs on their platforms, permitting investments into MFs via payment fintechs (albeit with caps on investment amount), easing rules for fintechs to become MF manufacturers (under its sandbox program) and much more.

Some obvious challenges in monetization and customer retention

Despite the opportunities, the wealthtech space has its own set of challenges, generating meaningful revenues being one of them. High competition has diminished distribution margins for new-age investment platforms, making it difficult to break even.

Consequently, most platforms have started expanding forward into becoming manufacturers of investment products. For eg, Zerodha has applied for an AMC license, Groww recently acquired Indiabulls AMC, Navi has applied for a license to cross-sell to its existing base of users, etc. Other platforms in Robo-Advisory etc. are also looking to apply for MF licenses.

Also, CAC is usually high in wealthtech due to higher compliance requirements and the need to for deeper customer understanding, and these platforms also have lower customer retention.

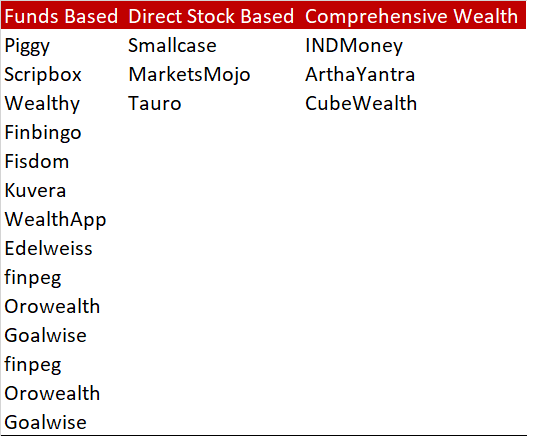

Indian Wealthtech Landscape

The following shows a detailed landscape of wealthtech in India.

Investor’s interest have been strongest in new age broking (easiest to generate revenues), followed by robo advisors. There has been recent interest in financial management products (Fello raised $1mn in Seed round, Akudo raised $4.2mn in seed round led by Y-Combinator). Piggy raised $500K in their seed round led by Y-Combinator as well.

I see interesting times ahead when a lot of these sub-segments will get bundled into super app kind of offerings.

Y-Combinator, Tiger Global. Accel, Sequoia, Ribbit Capital have been some of the most active investors in the space. Please see below for a detailed list of investments in the space.

Source: Abhishek Kumar

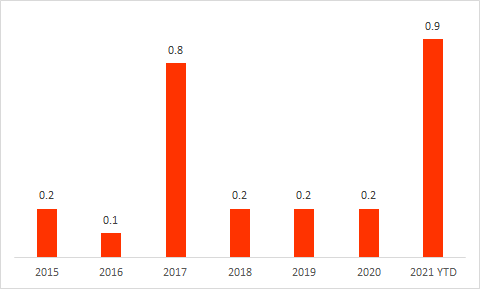

Overall, investment tech companies in India have raised US$2.4bn in funding since 2014. And 2021 is already the best year ever for the sector, with ~3 months to go.

Source :Tracxn, Abhishek Kumar

What are the top sub-segments to look out for?

New age brokers

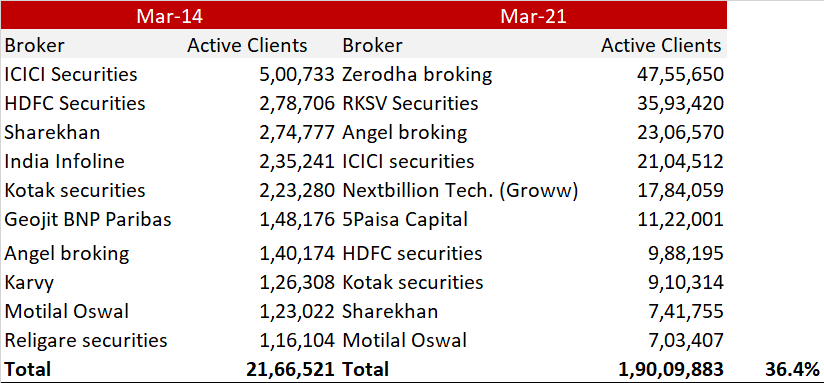

A majority of transactions in broking happen digitally, even for larger/ older players (where 90%+ transactions are originated digitally). Over the past 5-6 years, low-cost brokers have disrupted the market, capturing a lion’s share of broking volumes. Now, four out of top-10 and three out of top-5 brokers (by number of active customers on NSE) are low-cost brokers. None of these brokers were in the top-10 list seven years ago. These low-cost brokers now have ~60% share (of NSE's active customers among the top 10 players) and 47-50% overall.

Interestingly, since 2014, the industry, in terms of number of active people, has grown by a staggering 36.4% CAGR. Growth in terms of transactions is even higher at ~51% CAGR.

Source :Tracxn, Abhishek Kumar

Key drivers of this exponential growth are: 1) millennials becoming increasingly active in the equity markets (equity markets have seen strong inflows in both MFs and Direct Equities); 2) a general increase in equities investing, given the tax regime and government emphasis, vs. the earlier preference for hard assets such as gold and real estate. More importantly, the discount broking model has created a generation of users who are attracted to the lower cost offered as well as customised trading interface.

There's considerable variety among new-age platforms. A common thread is the desire to become a manufacturer of financial products via entry into the MF space; these players are more likely to take the passive/ ETF approach, which would keep costs low, would be easier for benchmarking and would not position them neck-to-neck with incumbents that enjoy strong brand positioning.

One difference is that some platforms like Zerodha have created platforms for active traders, with sophisticated tools; others, like Groww, are focusing on the mass segment that can be scaled up.

I also see lines blurring between the mainstream and digital/ low-cost platforms as both are converging in terms of prices, which may be a risk for new-age platforms. The incumbents are also tying up with platforms like bundled-investment platforms (like Smallcase, etc). Incumbents are now catching up with discount brokers in terms of pricing (Kotak is now cheaper than Zerodha!!). Interesting times ahead.

Cross-border investing

This is probably one area where I get the most queries - how does one invest in US stocks?

Now, there are platforms provide Indian investors access to global markets like the US, through tie-ups with foreign brokers using the LRS route (up to USD 250,000 per year).

These players offer investors options to invest in: (1) US-based stocks; (2) US-based ETFs; and (3) customized portfolios. Main sources of revenue are: (1) account opening and annual charges from Indian customers; (2) share of the broking commission; and (3) charges on AUM maintained.

Some of the top names in this sector are Vested (they offer fractional investments as well), SBINRI. Piggy also has a similar product in pipeline for this.

Robo Advisors

Roboadvisory is a form of investment management that uses algorithms to manage portfolios. It is suitable for retail portfolio management with mass customization. The process employs both quantitative and qualitative analysis to achieve the best possible investment performance.

Roboadvisory has been around since the 70s, but it has gone mainstream only recently, due to availability of advanced technology and cheap cloud infrastructure. The majority of robo advisors offer low-cost automated asset allocations and rebalancing services. The most common forms of roboadvisory services are automated investment advice, automated portfolio management and automated advice for retirement planning.

In a fully autonomous robo-advisory platform, customers typically answer a set of questions related to life stage, income/expenses, dependents, and future goals, based on which the algorithm can determine the risk-reward matrix and suitable portfolio commensurate to that matrix. The generated portfolio, then, can be reviewed by the customer and through integration with broking platforms, even orders can be placed and monitored.

Under the hybrid model, besides the robo-advisor, a professional investment advisor is assigned for a few days/hours, to assist customers. In addition to managing investments, robo-advisor services have expanded to include a variety of other financial decisions.

The future of these services is now focused on being able to provide automated financial guidance across investor lifecycle. Robo-advisory may include several parameters like currency hedging, asset class control, ability to select provide sectoral preference or whitelist/blacklist securities based on one’s preferences. Such robo-advisory platforms also offer complete DYI investment.

The key challenge these platforms face is the pressure on fees, especially with investors' preference to move towards direct mutual funds, discount brokers, etc. This is driving platforms to consider transitioning towards being manufacturers as well. This is why some of the platforms are considering/ applying for a license for mutual funds where they may offer ETF type of investment prospects.

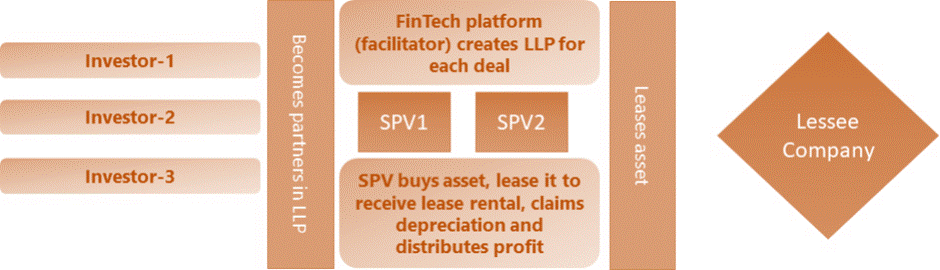

Fractional investments

Fractional investing allows people to pool money so that they can create a large enough corpus to invest in high-value assets or projects such as commercial real estate, hospitality, or sustainability-focused endeavours.

In the past couple of years, fractional investment in lease-based debt models through special purpose vehicle (SPV) in real estate and long-term asset classes have gained more popularity.

Fractional investing is now becoming more popular because they make asset classes more accessible with higher risk-adjusted returns than traditional asset classes. They offer pre-vetted investment options and provides good avenue for overall diversification.

Fractional Investing - How Does it work?

Source: Internet

Micro-saving

Micro savings refers to the concept of making very small investments in mutual funds, stocks and other asset classes through micro-savings apps like Acorn, Spenny, etc.

Whenever a user does a digital transaction, these platforms automatically invest the spare change in mutual funds, alternative investment assets, etc. For example, if customer spends Rs188 at a cafe, the app will round it up to Rs190, and that difference of Rs7 would be automatically invested into mutual funds.

All transactions that happen through the debit card / credit card or UPI apps like Google Pay, PhonePe, Paytm or even netbanking, can be rounded up and invested. Acorns, a pre-IPO start-up, made the concept of micro-savings popular in US and has grown to 4m users for its fintech and investment platform and aims to reach 10m by 2025.

Given that there are 356m young Indians in the 10-24 age group, changing demographics and growing interest in mutual funds, digital gold, etc amongst them, micro-savings will provide them with a good first-hand experience of investing in markets in a seamless and frictionless manner. Start-ups like Piggy, Spenny, Pennywise and Acru have recently floated similar products in India.

Money management

Money management apps provides users with a single dashboard of assets and liabilities. Apps like Indmoney, One Stack, Stack Finance, etc, provides a single platform where a user can save, spend, lend, and grow their money. Further, these apps generally, aggregate various financial products across financial providers, where users can compare multiple services and choose the one based on their individual preference.

What am I most excited about?

Products such as Piggy, which is combining multiple areas of wealthtech and brining banking services such as payments as well on one single platform is super exciting.

CredAvenue (I wrote about it earlier here) is also very exciting since it bridges the gap that debt financing in India always has. Something like Fello, which is attempting to bring in more users to investments are super exiciting.

What is for sure is that the SAM is huge here and there is space for multiple winners.

Hirings in Fintech

Highradius, a SaaS firm for treasury, O2C and record to report is hiring for multiple roles in product, tech and sales. Please reach out to me in case you are interested.

Dice is looking to hire for multiple roles, including growth head, partnerships and more. Please reach out to me in case you are interested.

Paytail is looking to hire for multiple positions, including growth and B2B marketing. Please reach out to me and will connect with the founders.

Xpresslane is looking to hire a Sales and Marketing Head. Super interesting role with good equity on offer. Reach out to me on abhishek@indiafintech.in and will connect with the founders.

Nimbbl is hiring for multiple positions. Reach out to co-founder, Anurag here.

M2P Fintech is hiring for multiple positions, including a product manager. Reach out to Franklin for this role.

Some of the interesting happenings in the Fintech Industry

Fintech startup Scripbox, a wealthtech management platform, raised $21 million in its Series D round via debt and equity from Accel Partners, and a bunch of other investors including Transpose Platform, the Sparkle Fund, InnoVen Capital, Trifecta Capital, KPB Family Trust, LetsVenture, and Kube VC, YY Capital.

Cholamandalam Investment and Finance Company has acquired a majority stake of 72.12% in Hyderabad-based online payment gateway startup Payswiff Technologies (Payswiff) for a sum of INR 450 Cr. Payswiff (earlier know as Paynear) offers omnichannel payment transaction solutions for businesses that help them accept payments from customers in-store, at home, while delivering using an mPOS (mobile point of sale), online and other POS solutions.

General insurance provider Digit Insurance has raised $70mn for its general insurance business from Wellington Hadley Harbor and Ithan Creek Master Investors.

INDmoney has raised $75 million in a new round as it attempts to build a super finance app to become a “one-stop shop” for people’s investments and expenses, a top executive said on Monday. Tiger Global, Steadview Capital, and Dragoneer co-led the startup’s $75 million Series D funding.

Rupifi has raised $25 million in a new financing round as the Indian startup, which currently provides buy now, pay later service to several marketplaces to serve their merchants, looks to expand its business-to-business payments offerings. Tiger Global, Bessemer Venture Partners, Quona Capital and Ankur Capital invested in this round.

Refyne, India’s first and largest earned wage access (EWA) platform, rasied $82 million (Rs 607 crore) in its Series B round led by Tiger Global, with significant contribution from existing international investors - QED Investors, partners of DST Global, Jigsaw VC, XYZ Capital, and RTP Global - and new investor Digital Horizon.

Youth-focused neobank Muvin has raised $3 million (around Rs 22.5 crore) as a part of its pre-Series A funding round led by WaterBridge Ventures, along with participation from Debt fund Alteria Capital and Krishna Bhupal, Co-Founder, Rational Pricing Technologies and board member of GVK Power & Infra.

Gold loan player Rupeek raised $34 Mn in a round led by Lightbox, GGV Capital and Bertelsmann, taking its valuation to $634 Mn.