Paytm and RBI – The dance of the Snake and the Mongoose | Episode 38

Paytm dodged RBI bullet many a times in the past. This time, it does look different.

Wow, what a week this has been in the Indian fintech space! With less than a pager of notification, RBI effectively killed not just the Paytm Payments bank, but also the wallet, fast tags, cards, processing UPI payments and much more. And in between the confusion, what got killed was the Paytm brand.

Imagine the plight of its ~40mn merchants, whose UPI scanner would be rendered invalid post Feb 29th this year. They process more than 100mn transactions monthly. After the RBI directive, the QR codes either need to be changed so that processing happens via other nodal banks or they need to be changed at backend. A tall task.

In addition, the way Payments and Payments Bank have been joined at the hip for Paytm (possibly the reason why RBI took the drastic step), the impact on the overall business is going to be massive. As per the company, a one-time EBITDA hit of Rs. 600 cr (One 97 communication, the parent company, lost Rs. 1,113 Crores in the trailing 12 months). If you go by various brokers, Payment bank is supposed to contribute ~40% of One 97’s revenues over the next 5 years. And then, there’s the issue of transferring revenues.

But that’s about financials. Let’s talk about what really happened, what could be the next steps for Paytm and if it can make a comeback.

PS – I hope they do, but the action on Paytm is not out of thin air.

Before you read ahead, please note that this blog is solely based on my views only. All views expressed here are my personal views and do not represent those of my employers, present or past. I do not own any Paytm shares and have never owned any.

What happened?

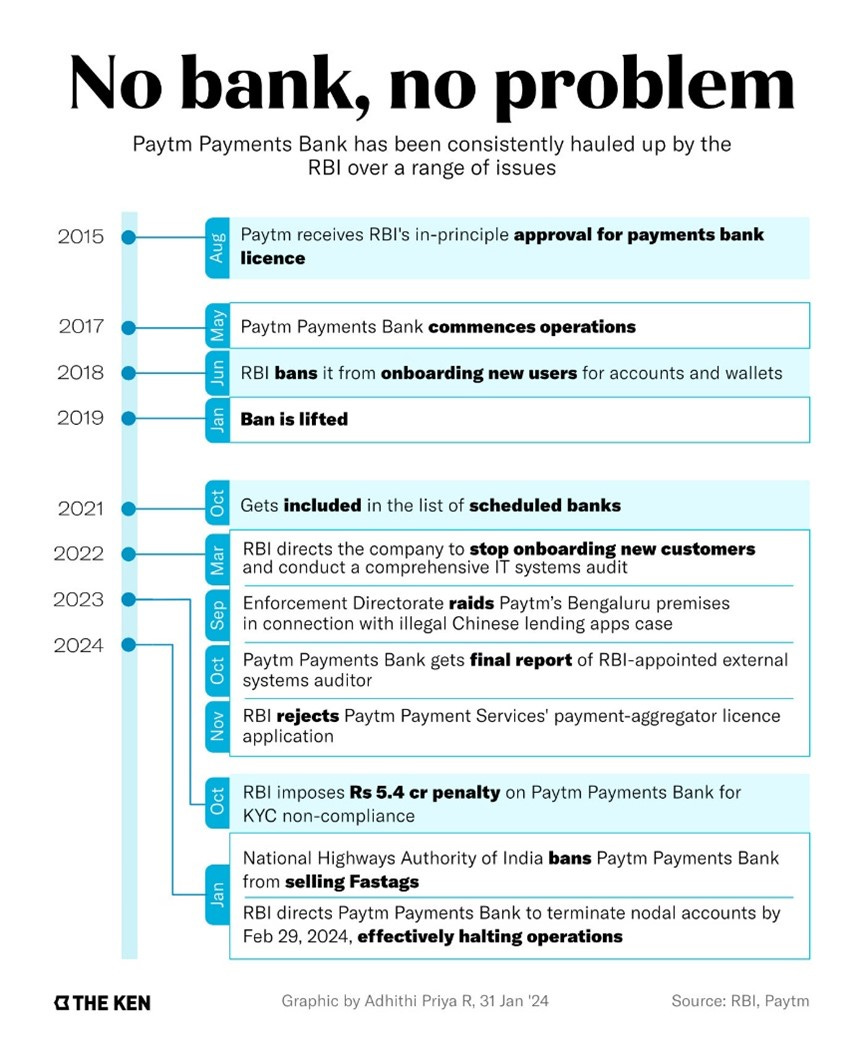

First, this timeline from one of the leading media agencies – Ken.

Almost every year since they started operations, RBI has been having issues with the payment bank business. In light of the above consistent issues, RBI’s action, though severe, was really not surprising or even unexpected. If anything, it follows at least five years of repeated warnings, audits and penalties. One may argue that Paytm, repeatedly, failed to pay heed to RBI warnings and went on about its business believing nothing will happen.

Fair it to say that the RBI ran out of patience and hope before it finally cracked the whip. It doesn’t really look like an overreach, which is what a lot of ecosystem players are trying to call this. After all, RBI did worse with State Bank of Mauritius or even Yes Bank or a whole lot of Co-operative banks and rightly so.

Interestingly, Bloomberg earlier reported that this could be a step towards cancelling the Payment’s bank license Worse, government agencies could also launch a full-scale probe into the company over possible money laundering charges (Paytm has denied charges as of now).

What are Paytm’s different businesses and what gets impacted immediately?

Paytm has a diversified revenue base, although it’s difficult to make out how much exactly comes from only Bank and bank related products. My earlier quoted number of ~40% in an estimation in that sense.

As it can be seen, there is high degree of overlap with almost every unit of Paytm with the payments bank and it’s like the Vecna in the Stranger things, spreading everywhere, but every part of the organization joined with everything else. Almost impossible to separate out parts.

So what gets impacted?

After 29 February, no transactions will be allowed using any of Paytm Bank’s products: its savings bank account, wallet, Fastag, or national common mobility cards. Withdrawal, though, will be permitted till the balance in these accounts lasts. The regulator also restricted the bank from facilitating any kind of transaction—including immediate payment service, Aadhaar-enabled payment system, and unified payments interface (UPI).

In short,

· It loses its wallet business, which has been its mainstay for years and the key entry point for almost all of its customers. Major, major hit. To continue wallets, they will have to now partner with a PPI issuer and in the process, they will lose out on the ownership of the customers.

· Also, it will lose its control of its UPI payment stack. So @paytm UPI ids will not be operational post 29th Feb. They can continue operating UPI using other banks stack, but it will be difficult to get these banks operationally ready this quick, especially given the RBI overhang. This also means services such as Credit card bill payment on paytm will go away.

· Fastags business, with ~1.5% take rate, will be hit. Paytm Payments Bank is the third-largest player in the Fastag eco-system. Users swear by the ease of use here and the sheer effort of tearing the tag up and putting a new one up is not going to be easy for millions.

· Now, it also loses its deposit franchise, which set it apart from rivals such as PhonePe, CRED, Razorpay and Pine Labs. This is a big hit, especially given their SFB ambitions.

· Other products such as National Common Mobility cards is also a goner.

· Due to ban on AEPS transfer, remittances business would also be hit.

But the biggest of all issues is this – In order to reroute the payment address from UPI payments to external banks, it needs to print 40mn+ QR Codes stickers and stick them by 29th February.

The key cause behind this massive impact is that Payment Bank’s operations are so deeply interlinked with its payments bank that it is difficult to say who does what. This interlinkage, while giving Paytm a competitive advantage, is also one of the issues flagged by the central bank. And going by industry insiders, this is what has pissed off the central bank.

Paytm has also paused it’s loan aggregation business for now, primarily because of concerns raised by lending partners around the scope of the RBI directives. Broking and insurance is a small part of the business and the impact is unclear in my view as of now. Of course, the payment aggregator license is still awaited (Competitors such as Cashfree, Razorpay, PhonePe have now got the nod to add new customers). Overall, the picture doesn’t look good.

And the stock markets agree. Stock price has fallen by ~40% since the RBI directives was made public. There was some recovery on 6th of Feb, but that’s about it

What does it look like and what is it, exactly?

On the face of it, it looks like RBI has acted because of Paytm’s inability to follow the KYC rules for its Payments bank business – 10,000 accounts using the same PAN card is an example. Various media channels have speculated the reason for this harsh directives due to lack of concrete reasons by RBI which in itself is a rarity.

Moneycontrol talked about Money laundering related party transactions. Tech Crunch talked about lack of Chinese walls between Paytm companies and unfettered data flow between them, thus flouting multiple rules.

There have been multiple violation of various service-level agreements in FASTag, as revealed in an audit by the National Highways Authority of India where Paytm Payments Bank reportedly refused to cooperate with the auditors. This one from TOI explores the issue.

It does boil down to multiple KYC violations, some inkling of Money Laundering, but most of all, Paytm’s inability to separate bank and payments business. That lack of arm’s length which made it impossible for users to figure out which entity served them, combined with multiple violations (including data breaches in their Video KYC infra), seems to be enough for the RBI to be this harsh.

What are my concerns here and what’s next for Paytm?

My biggest concerns are two folds here –

1) The RBI circulars and directives are usually prescriptive in nature, with the apex bank directionally looking to solve for issues. This doesn’t look to be the case here. This one looks like a final, non retractable kind of thing. Various brokers have said the same thing in as many words – They see this as effectively cancellation of Paytm’s Payment Banks license. And

2) Paytm’s board complete failure to anticipate this. In fact, they believed and were confident that RBI would validate their corrective actions. Couldn’t be more wrong! See here.

Now, if you think about the above, the issue that emerges is that Paytm is not prepared for what hit them. And 29 days is too less a time to solve these kind of issues. Paytm, broadly, needs to do the following, to stop the rout (not just the stock price, but mass exodus of employees, the good ones and overall operations)

1) They need to partner with multiple banks so that their customers and merchants continue to use their payments services. While there were some news of Yes Bank and ICICI being the favored banks, recent reports suggest it’s going to be difficult.

2) Get RBI’s nod for one-time migration of merchant accounts hosted by Paytm Payments Bank to other third-party banks to prevent any disruption. NPCI would be a key decision maker here.

3) Change the physical stickers on ~40mn merchants. This involves major effort, especially given the employees expectations around getting fired.

4) Figure out a way to separate payments and loan origination business from the bank’s business. This would be the toughest in my view.

All of the above will require humungous efforts, in an unnaturally short period. Sample this - All of Paytm’s 340 million+ wallet accounts as well as 150 million+ UPI handles are housed in the payments bank.

So, what’s next now and What are the implications for the startup ecosystem

Given the happenings around Byjus and now, Paytm, it doesn’t bode well for the Indian startup space. With RBI restrictions and regular tinkering on Payments (License issues), Digital Lending (Around FLDG and risk sharing) and now payments bank, the space does look like it’s filled with uncertainty. Add in the uncertainty around employment for tens of thousands employees, if not more and this could have a serious domino impact across the entire spectrum.

Fintech funding as it is have slowed in CY23 and RBI deliberately killing a large, scaled player is not going to instill confidence in both founders as well as the investors and this also opens up the Pandoras’ box of “What’s next ?”. The merits of why this was notwithstanding, this could have been handled better is what a lot of participants are thinking out loud.

A lot hinges on how Paytm reacts and how RBI takes this forward. Goona watch this space as much as you guys.

Please feel free to reach out to me at abhishek4ster@gmail.com for more discussions on fintech and financial services.