Reading Between the Lines: What RBI’s Latest Financial Stability Report Means for India’s Financial System | Episode 68

A lot of things are working. Some are in yellow zone

The latest RBI financial stability report (FSR) is an interesting read. Usually, I don’t dive deep into RBI’s periodic reports, primarily because they tend to oscillate between dry regulatory updates and politically cautious assessments that rarely move the needle for practitioners.

But the December 2025 Financial Stability Report is different. This isn’t just another semi-annual temperature check. It’s the RBI putting three clear risk markers on the table for anyone building, investing in, or regulating India’s financial system: asset quality pressures in specific lending segments, valuation risks in equities, and emerging vulnerabilities from stablecoins and private credit.

More importantly, the FSR reveals a fundamental tension that will shape the next 12-18 months: India’s financial system is structurally sound and well-capitalized, but pockets of stress are emerging precisely where growth has been most aggressive, especially unsecured retail lending, microfinance, and fintech-led credit.

For anyone in the fintech ecosystem, this report isn’t background reading. It’s probably a roadmap for where regulatory attention, capital allocation, and risk management priorities are headed.

I have tried to distill some of the directional things that the RBI is hinting at in this episode of Indiafintech. Let’s get to it.

The Big Picture: Resilience with Caveats

Let’s start with what’s working. India’s banking system today is in better shape than it’s been in over a decade. Capital adequacy ratios are comfortably above regulatory minimums, gross NPAs continue their downward march, and stress tests show banks can withstand even severe adverse scenarios.

The Tier 1 capital ratio for scheduled commercial banks stands at a healthy 14.1%, well above the 8% regulatory floor. Liquidity buffers are comfortable. Profitability metrics remain stable.

For context, this is night and day compared to 2016-17 when the banking sector was drowning in bad loans, capital was scarce, and every quarterly result brought new write-offs. The cleanup that started with the Asset Quality Review, followed by IBC implementation and capital infusions, has fundamentally repaired bank balance sheets.

But, and this is the critical nuance, aggregate health masks segment-level stress. The RBI is explicitly flagging three areas where vulnerabilities are building:

1. Unsecured Retail Lending: Growth Meets Reality

The unsecured personal loan market has been one of the fastest-growing segments in Indian lending. Digital lending platforms, fintech apps, and aggressive bank offerings have democratized access to credit in ways that were unimaginable five years ago. Personal loans grew at a CAGR of over 20% in the past three years, powered by instant approvals, minimal documentation, and slick user experiences.

The problem? Some of that growth came at the expense of underwriting discipline.

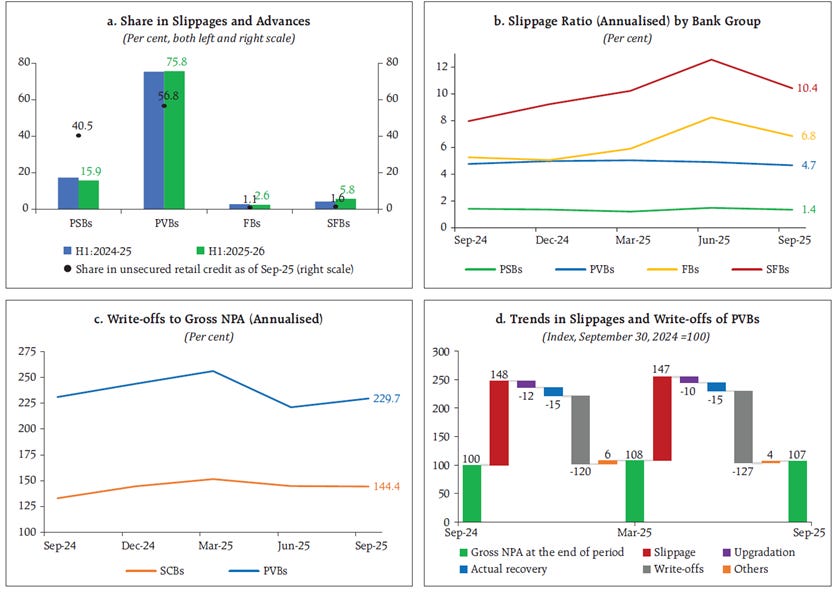

The FSR highlights rising slippages and write-offs in unsecured personal loans, particularly among private sector banks.

The chart from the report is telling. Private Sector Banks (PVBs) are seeing the highest share of slippages and advances in unsecured retail lending, with elevated write-off ratios compared to Public Sector Banks (PSBs) and Small Finance Banks (SFBs).

Source: RBI Financial Stability Report, December 2025

What’s happening here is a classic credit cycle pattern. When credit is easy and growth is the priority, lenders inevitably push down the credit curve, serving borrowers with thinner credit histories, lower income stability, and higher leverage. For a while, everything looks fine because defaults lag originations by 12-18 months. But when the cycle turns (economic slowdown, job losses, over-leveraging), those late-vintage loans start showing stress.

The RBI isn’t saying this is systemic yet. But it’s a clear yellow flag.

If you’re a lending fintech, a co-lending partner, or an investor in the space, this is the time to forensically examine portfolio quality, vintage performance, and collection efficiency. The days of growth at any cost are over. Underwriting discipline, robust collection infrastructure, and conservative provisioning will separate survivors from casualties.

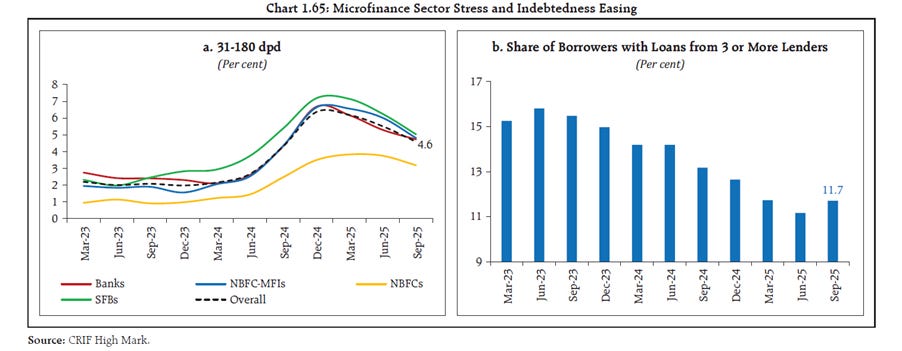

2. Microfinance: The NBFC-MFI Squeeze

Microfinance institutions have been another growth engine, particularly in serving underbanked rural and semi-urban customers. The MFI portfolio has grown steadily, driven by strong demand for small-ticket loans and relatively manageable NPAs during the post-pandemic recovery.

But the FSR flags rising credit costs and stress among NBFC-MFIs. Part of this is cyclical with rural incomes under pressure from uneven monsoons and slower agricultural growth. Part of it is structural: many MFI borrowers are now multi-leveraged, borrowing from multiple institutions simultaneously, which increases default correlation.

As seen above, share of borrowers with loans from 3 or more lenders has come down to ~11.7% from the highs of 16%+, but on an absolute basis, it remains high.

The other issue is the economics. NBFC-MFIs operate on thin margins, high operating costs (due to field-based collection models), and are vulnerable to funding cost spikes. Unlike banks, they don’t have low-cost CASA deposits. They’re reliant on bank borrowings, bonds, and securitization, all of which reprice quickly when liquidity tightens or risk appetite falls.

For fintech players in the microfinance or small-ticket lending space, the message is clear: you need more than just a tech-enabled disbursement model. You need defensible unit economics, access to stable and diversified funding, and collection mechanisms that work in stress scenarios.

The next 12 months will test which models have real resilience versus which ones were just riding a benign credit environment.

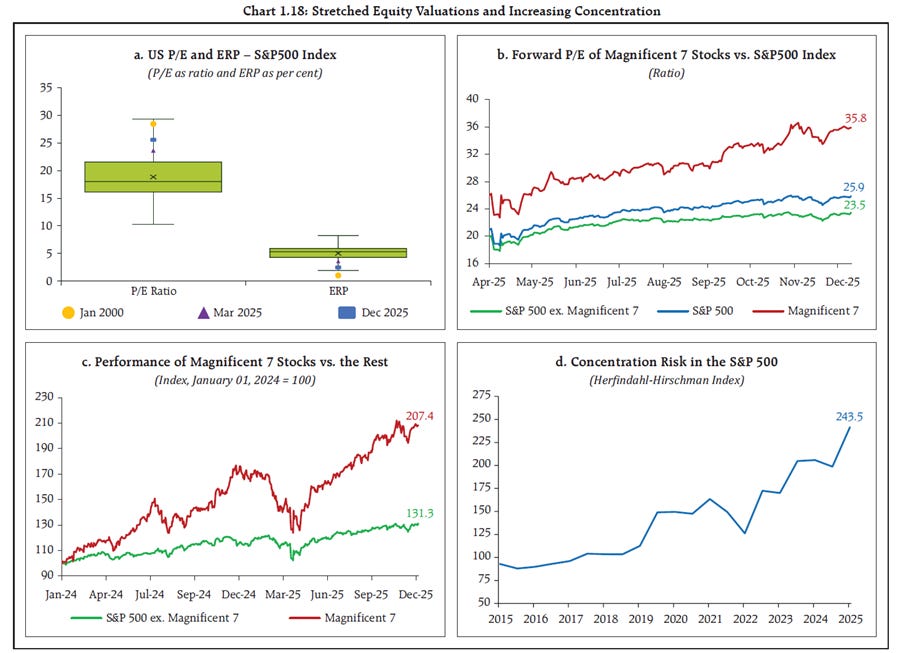

3. Valuation Risk in Equities: The AI Bubble Question

The second major risk the RBI flags is equity market valuations. Global equity markets, and to a smaller extent, Indian markets, have been on a tear, driven largely by AI optimism and a narrow set of mega-cap tech stocks. The S&P 500, Nasdaq, and even Nifty have scaled new highs despite elevated uncertainty.

The FSR notes that valuations are at the higher end of historical ranges, with a small set of stocks (AI-linked names) accounting for a disproportionate share of returns. This concentration creates fragility. If sentiment shifts, say, AI doesn’t deliver on its productivity promises, or earnings disappoint, the correction could be sharp and broad-based.

It’s actually surprising how much the RBI report talks about the valuation risk of US based markets, especially the top 7 stocks: Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. It does look like everyone is watching these and the ripple effects are much more spread than initially thought of.

Source: RBI FSR Report

For India, the risk is more about spillovers than domestic fundamentals. Indian equities have been supported by strong SIP inflows, resilient corporate earnings, and foreign inflows returning after a hiatus. But if US markets correct sharply, emerging markets including India will feel the heat through portfolio rebalancing, FPI outflows, and tighter financial conditions.

The FSR’s broader point is that markets are pricing in perfection. However, equity risk premiums are compressed. Bond spreads are tight. Volatility is low.

All of this suggests that when the correction comes (not if, but when), it could be disorderly. For fintechs in wealth management, broking, or capital markets infra, this is a reminder to stress-test for liquidity crunches, margin calls, and sharp swings in customer behavior.

The New Frontier: Stablecoins and Private Credit

One of the most forward-looking sections of the FSR is the special feature on stablecoins, a topic that’s typically absent from central bank reports in India.

The RBI’s inclusion of these signals growing attention to crypto-linked financial stability risks.

Stablecoins have grown explosively, now representing over $200 billion in global market cap. They’re deeply integrated into crypto trading, cross-border remittances, and decentralized finance (DeFi) ecosystems. The stability promise1 stablecoin = $1, depends on reserves held by issuers, typically in US Treasuries or cash equivalents.

The FSR flags three risks:

Run Risk: In stress events, mass redemptions of stablecoins could force issuers to liquidate Treasury holdings rapidly, amplifying liquidity shocks in sovereign bond markets.

Interconnectedness: Stablecoins are increasingly used as collateral, margin, and settlement assets across crypto and traditional finance. Failure or de-pegging of a major stablecoin could cascade through the system.

Regulatory Arbitrage: Many stablecoin issuers operate in lightly-regulated jurisdictions, creating opacity around reserve quality, leverage, and governance.

For India, direct exposure is limited since crypto adoption is relatively niche, and stablecoin usage is primarily offshore. But the spillover risks are real. If a global stablecoin crisis triggers broader deleveraging or liquidity tightening, Indian markets won’t be immune.

The other emerging risk the RBI highlights is private credit, opaque lending structures, often structured as pass-through vehicles or AIFs, that sit outside traditional banking regulation. Global private credit markets have ballooned to over $1.5 trillion, and Indian banks are increasingly providing warehousing credit or investing in these vehicles.

The concern is straightforward here. If these credit structures face losses (which are inevitable in a downturn), and banks have exposure via multiple channels, the transmission of stress could be faster and more opaque than traditional loan losses. This is an area where regulatory scrutiny will only intensify.

What This Means for Indian Fintech

If you’re building or investing in fintech, here’s what the RBI is telling most likely:

Growth discipline matters more than growth rate. The unsecured lending and MFI stress signals are clear: regulators are watching, and the market is punishing poor underwriting. If your model depends on aggressive customer acquisition, loose underwriting, or high leverage, now is the time to recalibrate.

Funding diversification is existential. NBFC-MFIs are struggling partly because their funding is expensive and concentrated. Fintech lenders need to build multiple funding channels—bank partnerships, securitization, bond markets, equity—and ensure they’re not dependent on one or two sources.

Transparency and governance will be differentiators. Whether it’s private credit, stablecoins, or digital lending, the RBI is signaling that opacity creates systemic risk. Companies that embrace transparency, strong governance, and proactive regulatory engagement will earn trust and capital access.

Prepare for volatility. Equity market corrections, currency swings, and liquidity tightening are on the horizon. If your business model assumes benign markets, smooth funding, and perpetual risk-on sentiment, you’re vulnerable. Build buffers, stress-test for adverse scenarios, and maintain operational flexibility.

Play the long game. The Indian fintech opportunity is massive and durable. But the next phase won’t be about blitzscaling or subsidy-driven growth. It’ll be about building sustainable unit economics, earning customer trust through consistency, and navigating regulatory evolution with maturity.

The FSR is essentially saying: the system is strong, but excesses will be corrected. Position yourself on the right side of that correction.

Regulatory Implications: What’s Coming

The FSR doesn’t just diagnose risks, it telegraphs where regulatory action will focus. Expect the following in the next 12-18 months:

Tighter norms on unsecured lending: Risk weights might go up, evergreening will face scrutiny, and lenders with weak collection practices will be flagged.

Enhanced oversight of NBFC-MFIs: The RBI will likely introduce stricter limits on borrower leverage, collection practices, and MFI exposure caps for banks.

Crypto and stablecoin regulations: While India doesn’t yet have a stablecoin framework, the FSR’s inclusion suggests work is underway. Expect either an outright ban or a tightly controlled permissioned model.

Private credit transparency: Banks’ exposure to AIFs and pass-through structures will face tighter disclosure and concentration limits.

Market volatility preparedness: SEBI and RBI will coordinate on margin frameworks, circuit breakers, and stress-testing for brokers and clearing members to handle sharp corrections.

For fintech founders and investors, the key is to engage with these shifts proactively. Waiting for draft regulations to be released is probably too late. The time to build compliant, transparent, and resilient businesses is now.

Bottomline

The December 2025 FSR is ultimately a story about maturity. India’s financial system has graduated from crisis management (2015-18) to stability maintenance (2019-24) to selective risk surveillance (2025-26). The system is strong enough to absorb shocks, but specific segments are showing froth that needs correction before it becomes systemic.

For fintech, this is both sobering and clarifying. The era of growth-at-any-cost, regulatory arbitrage, and valuation momentum is closing. The next era will reward companies that combine technological innovation with financial discipline, customer empathy with underwriting rigor, and ambition with transparency.

The RBI has done its job and flagged the risks clearly, without panic or overreach. Now it’s on the ecosystem players: builders, investors and operators to take these warnings seriously and build businesses that don’t just ride the upcycle but endure through complete cycles.

Disclaimer: The views presented here are my own and do not reflect the views of my employer in any way. This should not be construed as investment advice. Please consult a qualified investment advisor before making any financial decisions.

It's interesting how you distiled this FSR. Pinpointing the tension between resilience and aggressive growth is insightful. This feels like a global heads-up, beyond India. With AI accelerating financial trends, these stress points could be early warnings for many economies.