The Challengers : A Deep Dive Into India’s NBFC Landscape | Episode 78

India’s non-banking financial companies are at a fascinating inflection point. The old guard is transforming, the challengers are scaling, and the line between banks and NBFCs is blurring fast.

There’s a peculiar irony at the heart of Indian finance. The country has over 9,000 NBFCs registered with the RBI, yet the conversation almost always narrows down to a handful of names. Bajaj Finance. Shriram. Mahindra Finance. Maybe a Poonawalla or Five Star if you’re paying close attention. The rest fade into the background noise of quarterly earnings calls and brokerage reports that few people actually read.

The NBFC story in India has never really been about the names, though. It is about the architecture of credit delivery in a country where formal banking still doesn’t reach large swathes of the population. A farmer in Andhra Pradesh or a small kirana store owner in Tier-3 Maharashtra still finds it easier to walk into an NBFC branch than to navigate the labyrinthine loan application process of a large bank.

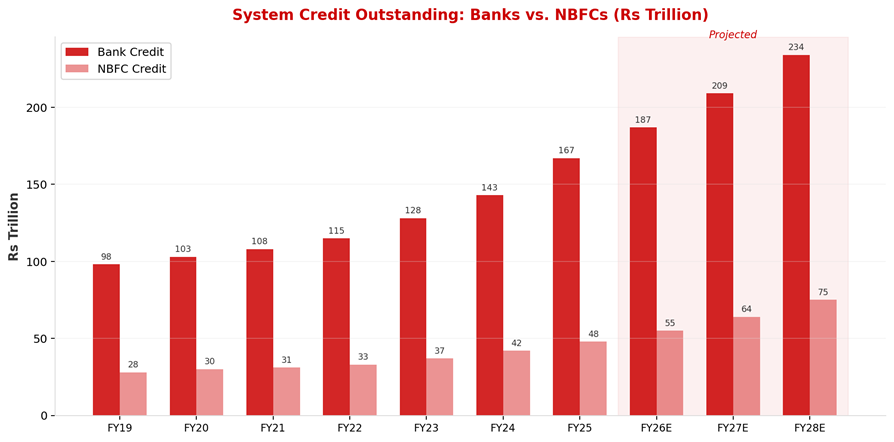

Banks remain the cornerstone of India’s lending landscape, accounting for over 70% of total system credit as of FY25. Between FY19 and FY25, credit expansion across the banking system trailed NBFC growth by a relatively narrow margin of around 200 basis points. That said, a fresh wave of ambition is sweeping through the NBFC space, fueled in part by seasoned banking professionals who have migrated to these firms in recent years.

Beyond chasing new product lines or untapped geographies, NBFCs are actively building AI-driven capabilities that could reshape how lending operates across the industry. Conversations with industry participants show a growing belief that artificial intelligence can help NBFCs identify creditworthy borrowers more effectively and deliver step-change improvements in operationally demanding product categories. The data I’m seeing from portfolio companies and the broader ecosystem backs this up: AI-driven underwriting models are delivering measurable improvements in approval rates and credit costs simultaneously, something that would have been considered a contradiction five years ago.

Industry participants anticipate that this momentum will widen the growth differential between NBFCs and banks, with NBFCs projected to deliver roughly 18% annualized loan growth over FY25-35F, compared to about 12% for banks.

System Credit Outstanding: Banks vs. NBFCs, FY19-FY28E (Rs Trillion)

Source: RBI, Company data, Author’s estimates

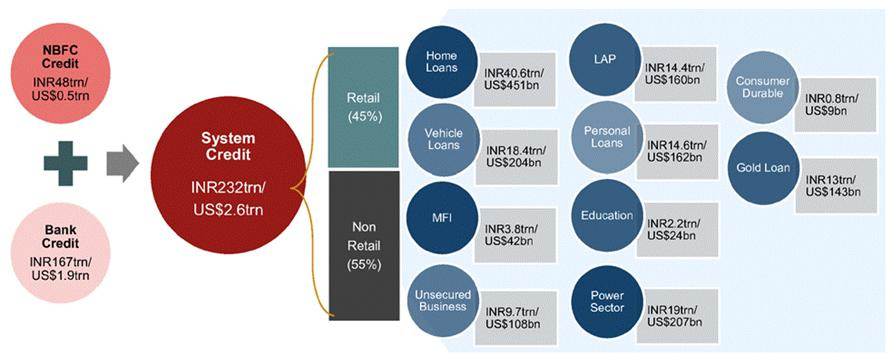

The following captures the overall system credit architecture in the country:

Source: Company data

The big picture: NBFCs in numbers

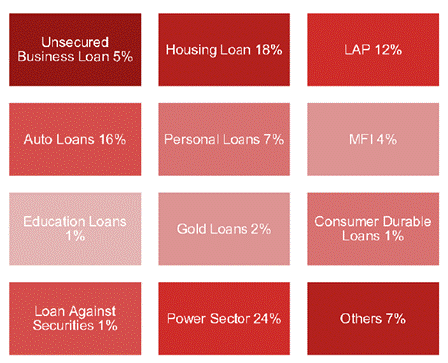

The total NBFC credit outstanding has grown at a roughly 15-17% CAGR over the past five years, consistently outpacing the banking system’s credit growth. NBFCs have evolved well beyond their gap-filler origins. They’ve become genuine competitors to banks across several product segments, with vehicle finance, affordable housing, gold loans, and small-business lending as the key segments.

To put this in perspective, consider the trajectory. NBFC credit as a share of total system credit has crept up from ~15% in FY18 to ~18% in FY25. On an absolute basis, the sector’s AUM now exceeds Rs 45 lakh crore. And the growth is accelerating in the segments where banks have structural disadvantages: pre-owned vehicle assessment, last-mile housing construction finance, micro-enterprise working capital, and gold-backed liquidity for agricultural households.

NBFC Loan Mix by Segment, FY25

Source: RBI, Company data

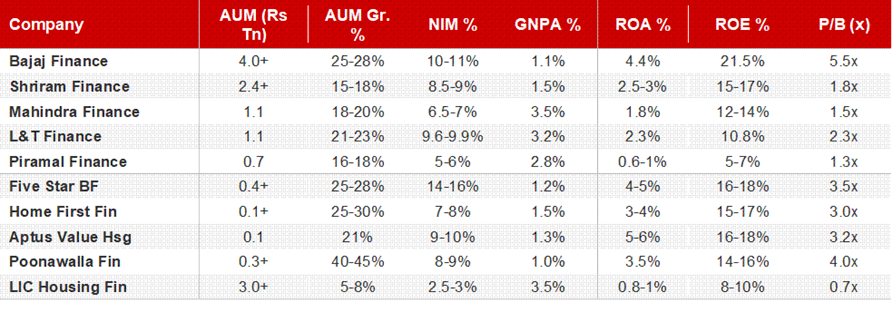

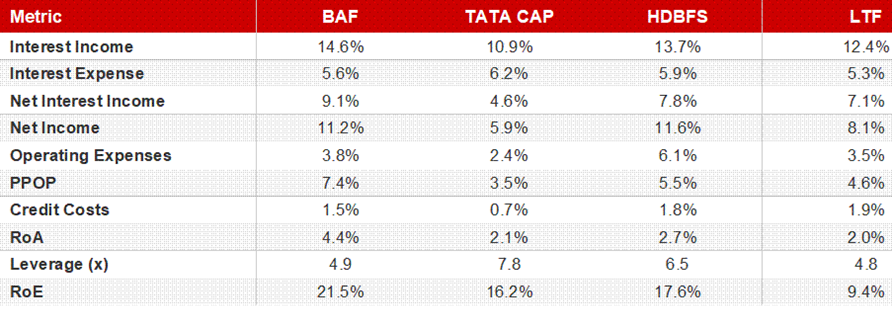

Key NBFC Metrics Snapshot: Select Listed Players (FY25/Latest)

Source: Company data, Nomura estimates; Kotak Institutional Equities

Banks vs. NBFCs: The structural tug of war

One of the most consequential trends in Indian financial services over the past five years has been banks’ aggressive push into retail lending segments traditionally the domain of NBFCs. HDFC Bank (post-merger), ICICI Bank, and even SBI have been deploying capital and technology into vehicle finance, affordable housing, and small-ticket personal loans with a ferocity that’s forcing NBFCs to rethink their positioning.

The advantage banks hold is simple and powerful: cost of funds. A large private bank can raise deposits at 6-6.5%, while an AAA-rated NBFC pays 7-8% for its borrowings. That 100-150 basis point differential is enormous in a business where net interest margins are the primary driver of profitability.

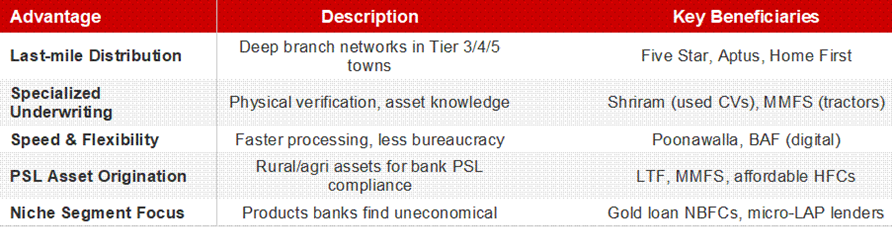

NBFCs retain significant advantages in three areas, though. First, last-mile distribution: Five Star’s deep presence in Tier-3/4 towns, where the nearest bank branch might be 30 kilometres away. Second, specialized underwriting: Shriram’s pre-owned CV assessment capabilities built over four decades, which require physical inspection and market knowledge that no centralized credit algorithm can replicate. Third, speed and flexibility: Poonawalla’s ability to disburse personal loans in hours, compared to the multi-day processes at most banks.

In conversations with NBFC management teams over the past quarter, I’ve heard a consistent refrain: the real competitive moat for NBFCs going forward is neither distribution nor cost, but data-driven underwriting in segments where traditional bureau scores don’t work. If you’re lending Rs 7 lakh against a piece of land in rural Tamil Nadu, your CIBIL score tells you almost nothing. The NBFC that can assess the borrower’s repayment capacity using field data, satellite imagery, and transaction patterns has a genuine structural edge.

Cost of Funds Pecking Order: Banks vs. NBFCs

Source: Company data, own estimates

Structural Advantages: Where NBFCs Still Win

Source: Company data, own estimates

The marquee names: individual profiles

Bajaj Finance: Still the gold standard?

No discussion of Indian NBFCs is complete without addressing the 800-pound gorilla in the room. Bajaj Finance, with its AUM crossing Rs 4 trillion, remains the sector benchmark. Under Rajeev Jain’s leadership, BAF has transformed from a consumer durables financier into a diversified lending platform spanning two-wheeler loans to commercial real estate.

The numbers are remarkably strong: ROA consistently above 4%, ROE north of 20%, and a cost-to-income ratio that most banks would envy. However, BAF’s AUM growth has moderated to 25-28%, down from 30%+ levels. Credit costs have inched up. The more fundamental question is whether it can sustain premium valuations (currently ~5x book, median of 7.8x over the last 10 years or so) as growth moderates and the competitive landscape intensifies. At some point, the law of large numbers catches up with even the best-run platforms.

Shriram Finance: The quiet compounder

If Bajaj Finance is the glamorous headline act, Shriram Finance is the steady rhythm section. The merger of Shriram Transport Finance with Shriram City Union Finance created a diversified platform with AUM exceeding Rs 2.4 trillion. Shriram’s pre-owned commercial vehicle financing franchise is a strong business model in India’s lending landscape, built over four decades with 2,500+ branches and deep local market knowledge.

Post-merger, they witness combined AUM growth of 15-18%, NIMs holding firm at 8.5-9%, and credit costs remaining remarkably stable. The Shriram story is a bet on India’s logistics backbone continuing to expand. As long as goods move on trucks in India (and that’s a very long time), Shriram will have a business.

The Housing Finance brigade: Building India, one Rs 10 lakh loan at a time

Affordable housing finance companies have been compounding at 20-30% AUM growth rates, serving a massive market largely ignored by large banks. The typical borrower in this segment owns 1,000-1,500 sq ft of land, needs Rs 7-10 lakh for construction, and works as a kirana store owner, contractor, or agricultural labourer.

These borrowers don’t have salary slips or ITRs. Income assessment involves physical field visits, review of land ownership documents, inspection of jewelry holdings, and examination of chit fund participation patterns. The fact that companies like Aptus run a GNPA ratio below 1.5% while lending to this segment is a testament to the quality of their on-ground underwriting processes.

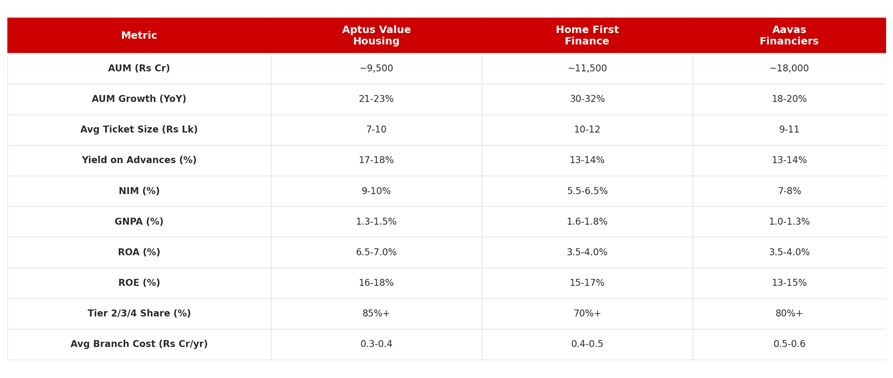

The three players worth tracking closely are Aptus Value Housing, Home First Finance, and Aavas Financiers, each with a distinct approach to the same market.

Affordable Housing Finance: Comparative Metrics (FY25/Latest)

Source: Company data, broker estimates

Aptus stands out for its extraordinary yield profile, charging 17-18% on affordable housing loans. This is possible because the borrower profile is inherently self-selecting: these are people who have no alternative source of formal credit. The trade-off is that competition is now arriving. Aptus management noted that peers are undercutting on LTVs and FOIRs. Pre-closures run at 7.5%, and buyout rates from banks sit at 4-5%. Aptus has moderated growth guidance from 25% to 21% and reduced exposure to tickets below Rs 0.7 million.

Home First, by contrast, operates at a lower yield (13-14%) but with higher volumes and slightly larger ticket sizes. Its growth rate is the fastest in this cohort, at 30%+, driven by a tech-enabled origination platform that has been particularly effective in Gujarat and Maharashtra. Aavas, the oldest of the three, has the most conservative approach: slower growth, the lowest GNPAs, and a diversified geographic spread.

The key risk across this entire segment is the threat of a buyout. As banks push deeper into affordable housing (driven by PSL requirements and improved rural reach through digital channels), the best borrowers in these portfolios will be cherry-picked. NBFCs will be left with the residual pool, which, unless underwriting adapts, could lead to deteriorating asset quality over time.

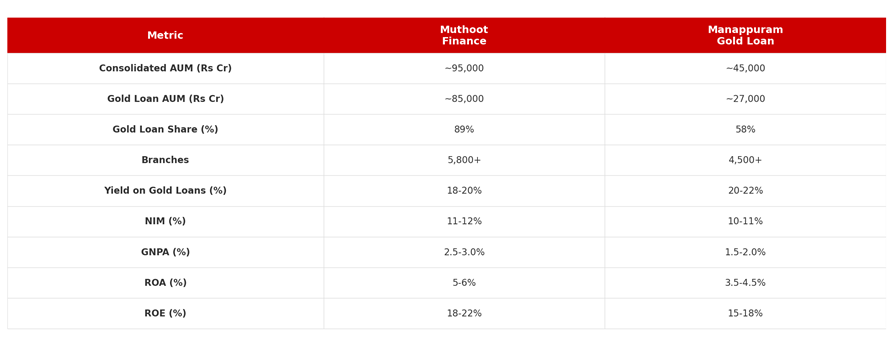

The gold loan powerhouses: Muthoot and Manappuram

No landscape piece on Indian NBFCs would be complete without covering the gold loan segment, and the two companies that dominate it. Muthoot Finance and Manappuram Gold Loan together hold over Rs 1.5 lakh crore in gold-backed AUM, making this one of the largest NBFC sub-segments by asset size.

The gold loan business model is, at its core, one of the most elegant lending structures in financial services. The collateral is liquid, fungible, and has a globally traded price. LTVs are capped at 75% by the RBI. Auctions are straightforward if the borrower defaults. Credit losses are negligible, typically below 0.5% of AUM. The result is a business with ROAs of 4-6%, minimal credit costs, and almost no asset-quality volatility across economic cycles.

Muthoot Finance is the undisputed leader with a consolidated gold loan AUM exceeding Rs 85,000 crore. The company operates through 5,800+ branches, primarily in South India, though it has been expanding aggressively in the North and West. The franchise is old, tracing its roots back to 1887 in Kerala. NIMs run at 11-12%, and the ROA has consistently been in the 5-6% range.

Manappuram is the number two player with gold loan AUM of roughly Rs 25,000-27,000 crore. What makes Manappuram more interesting from an analyst’s perspective is its diversification story. Under VP Nandakumar’s leadership, the company has deliberately expanded into microfinance (through Asirvad Microfinance), vehicle finance, and affordable housing. Gold loans now account for roughly 55-60% of consolidated AUM, down from 90%+ a decade ago.

Gold Loan NBFC Comparison (FY25/Latest)

Source: Company data

The structural tailwind for gold loan NBFCs is India’s gold stock: estimated at over 25,000 tonnes, worth roughly $1.8-2.0 trillion. Only a fraction of this is currently monetized through formal lending channels. Every percentage point increase in gold monetization represents an addressable market expansion of $18-20 billion.

The risk to this segment is primarily competition. Banks have been aggressively entering gold lending (SBI, Federal Bank, CSB Bank, and South Indian Bank all have significant gold loan portfolios). Online gold loans, pioneered by Rupeek and more recently by platforms like Muthoot Online, are compressing turnaround times. The question is whether the branch-heavy model of traditional gold NBFCs will be disrupted by digital-first approaches, or whether the physical inspection of gold and the trust relationship with the borrower remain non-negotiable.

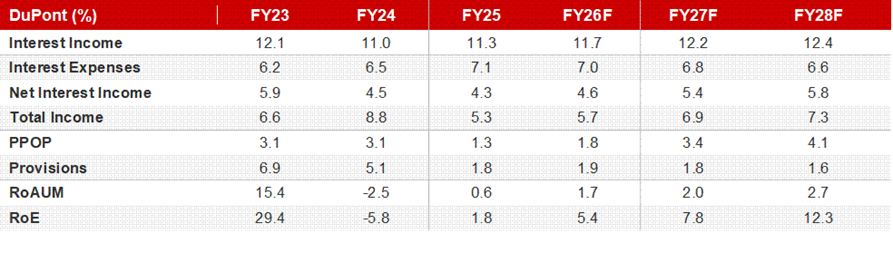

Piramal Finance: The turnaround story

There’s something almost novelistic about the Piramal Finance story. Entered financial services in 2012 through wholesale real estate lending, rode the boom, got caught in the IL&FS and Covid crises, acquired the troubled DHFL book, and is now reinventing itself as a retail lending platform. One could make a redemption movie on this!

Piramal Finance: DuPont Analysis (% of Average Assets)

Source: Company data, broker’s estimates

The board and management team is genuinely intriguing: Jairam Sridharan (former Axis Bank) as MD & CEO, Shikha Sharma (former Axis Bank CEO) on the board, Anjali Bansal (Avaana Capital founder), and Nitin Nohria (former Dean of Harvard Business School). Management has guided for 3% ROA at the terminal state. Reaching that from the current ~1.5-1.8% requires a meaningful shift in both mix (more retail, less wholesale) and cost efficiency (opex/assets needs to come down by 50-70 bps). I’m watching the quarterly trajectory on this one closely.

L&T Finance: From wholesale to retail, powered by AI

The L&T Finance transformation is the most instructive case study of how an Indian NBFC can reinvent itself. In 2016, LTF’s loan book was 66% wholesale, primarily infrastructure and real estate. By December 2025, retail loans constituted 98% of the book. The company went through IL&FS, Covid, and the 2024-25 MFI stress. AUM between FY20-23 actually declined as it deliberately ran down wholesale.

L&T Finance: Loan Mix Evolution, Wholesale to Retail

Source: Company data

Lakshya 2026: Targets vs. Achievements

Source: Company data

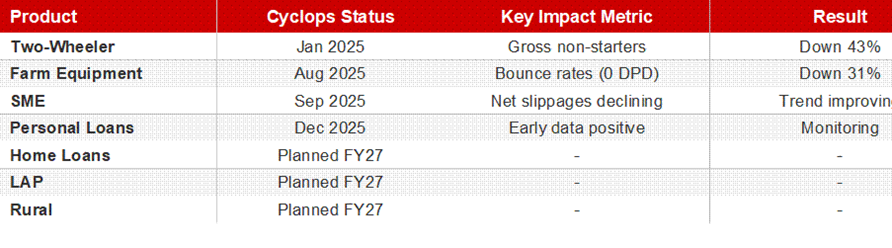

The AI stack is what makes LTF genuinely fascinating. The company has built two proprietary systems: Cyclops (AI-based underwriting engine) and Nostradamus (portfolio monitoring engine), which are fundamentally changing how it underwrites and monitors loans.

The Cyclops system processes over 100,000 data variables per application for two-wheeler loans. The result is impressive! LTF’s approval rate improved by 15%+ while simultaneously reducing credit costs.

Nostradamus provides early warning signals on portfolio stress, enabling proactive collections before accounts slip into delinquency. For anyone who thinks AI in BFSI is still a PowerPoint exercise, LTF is the counter-example.

L&T Finance AI Stack: Cyclops Implementation Timeline & Impact

Source: Company data

Average ROE Tree (FY23-25): L&T Finance vs. Peers (% of avg assets)

Source: Company data

The Microfinance minefield

The MFI sector went through a man-made crisis in 2024-25. Customer leverage peaked as multiple lenders chased the same borrower pools in overlapping geographies. Delinquencies spiked. PAR 31-90 days shot up to 6-9% at some of the largest players. PAR 90+ at some companies reached 12-13%.

MFI Performance During the 2024-25 Crisis: PAR Comparison (3QFY26)

Source: Company data

L&T Finance came through with PAR 31-90 of 0.8-1.0% and PAR 90+ around 2.6-2.7%, significantly better than peers. LTF credits its self-imposed three-lender cap (since 2019) and technology-driven income assessment for the outperformance.

The broader takeaway is that microfinance in India operates in a structural tension between genuine credit needs and lender over-servicing during booms. The RBI’s guardrails (income caps, lending caps per borrower, pricing transparency requirements introduced in late 2024) are necessary correctives. The players who survive will be those with disciplined geographic diversification and a willingness to throttle growth when portfolio indicators deteriorate.

MFI is a business where the best cycles plant the seeds of the worst ones. And probably, vice-versa.

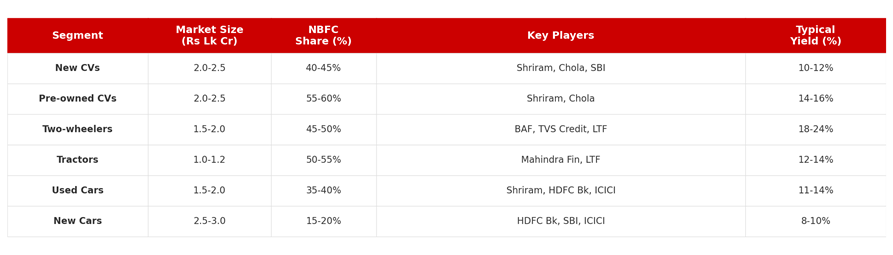

Vehicle Finance: India’s Rs 10 lakh crore lending backbone

India’s vehicle finance market is one of the largest NBFC segments, with total outstanding credit estimated at Rs 10-12 lakh crore across all vehicle types. NBFCs dominate the non-new-car segments, holding an estimated 55-60% market share in used commercial vehicles, 45-50% in two-wheelers, and 35-40% in used cars. New car financing remains bank-dominated, with HDFC Bank, SBI, and ICICI Bank holding the lion’s share.

The segment breaks down into distinct sub-markets, each with its own economics.

Commercial vehicles (new and pre-owned) represent the largest single pool, with outstanding credit of roughly Rs 4-5 lakh crore. Shriram Finance’s pre-owned CV franchise, built over four decades, requires physical inspection and deep local market knowledge that algorithms can’t fully replicate. Every used truck has a different story: mileage, maintenance history, route history, driver profile, and resale value. Shriram’s 2,500+ branches with local assessors who know the specific vehicle markets in their regions represent a genuine moat. Yields on pre-owned CVs run at 14-16%, with credit costs of 2-3%, delivering attractive unit economics.

Two-wheeler financing is the high-volume, small-ticket segment, with typical ticket sizes of Rs 60,000-1,50,000 and enormous monthly disbursement volumes. This is where LTF’s Cyclops AI engine was deployed first, precisely because the combination of small ticket size and high volume makes automated underwriting essential for profitability. Bajaj Finance and TVS Credit are also significant players here. Yields range from 18-24%, but credit costs can spike during economic downturns because two-wheeler borrowers tend to be more vulnerable to income shocks.

Tractor financing is inherently seasonal, tied to monsoons and agricultural cycles, with yields of 12-14% and a borrower profile that overlaps significantly with the affordable housing and gold loan segments. Mahindra Finance has the largest franchise here, leveraging Mahindra’s dealer network for origination.

The used car segment is formalizing rapidly through platforms like Cars24, Spinny, and CarDekho, creating new organized lending opportunities. This is a segment where NBFCs and banks compete more directly. The formalization trend is positive for lenders because it improves vehicle documentation and price discovery, reducing the information asymmetry that has historically made used-car lending riskier.

Vehicle Finance Market Size by Segment (FY25E)

Source: Industry estimates, company data

The structural tailwind is simple. The country has roughly 35 crore registered vehicles, with an annual addition rate of 8-10%. As the economy formalizes and logistics demand increases (driven by e-commerce, last-mile delivery, and infrastructure spending), vehicle finance will remain a multi-decade growth story.

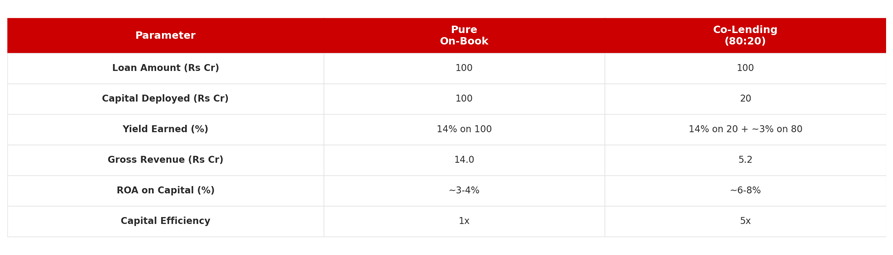

Co-Lending and Securitization: The hidden plumbing of NBFC growth

Co-lending has been one of the most significant structural shifts in Indian financial services over the past three years, and its economics deserve a proper treatment.

The structure is straightforward here. The NBFC originates and underwrites the loan, retains 20% on its own balance sheet, and the partner bank funds the remaining 80%. The NBFC earns a spread (typically 2-3% on the bank’s portion) plus a servicing fee. The bank gets access to borrower segments it couldn’t reach through its own branch network. For the NBFC, the math is compelling: 5x origination volume per unit of capital deployed.

Co-lending volumes have grown explosively, crossing Rs 1 lakh crore in cumulative disbursements during FY25. The top co-lending pairs include SBI-L&T Finance, Union Bank-Five Star, and Bank of Baroda-Poonawalla. SBI alone has active co-lending arrangements with over 15 NBFCs.

Co-Lending vs. On-Book Lending: The ROA Math

Source: Author’s estimates

The trade-off is margin compression on the co-lent portion. The NBFC gives up significant NIM in exchange for capital efficiency. And there’s a governance risk: if the bank’s credit appetite shrinks during a downturn, the NBFC is left holding the pipeline without a funding partner.

Securitization is the other hidden plumbing mechanism. It provides NBFCs with funding diversification, capital efficiency, and PSL arbitrage (rural and housing loans that qualify as priority sector lending command a premium from banks). LTF’s bank loans toward PSL assets rose from 16% of the borrowing mix in FY23 to 26% in 3QFY26, a deliberate strategy to lower funding costs.

Direct Assignment (DA) and Pass-Through Certificate (PTC) volumes have both been growing at 20%+ annually. The securitization market in India crossed Rs 1.8 lakh crore in FY25, with vehicle loans and housing loans accounting for the bulk. For NBFCs with strong origination engines, securitization effectively transforms them into origination-and-servicing platforms that don’t need to hold credit risk on the balance sheet permanently.

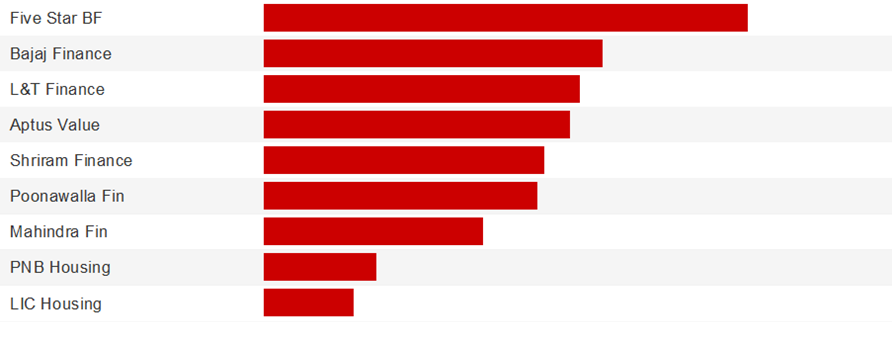

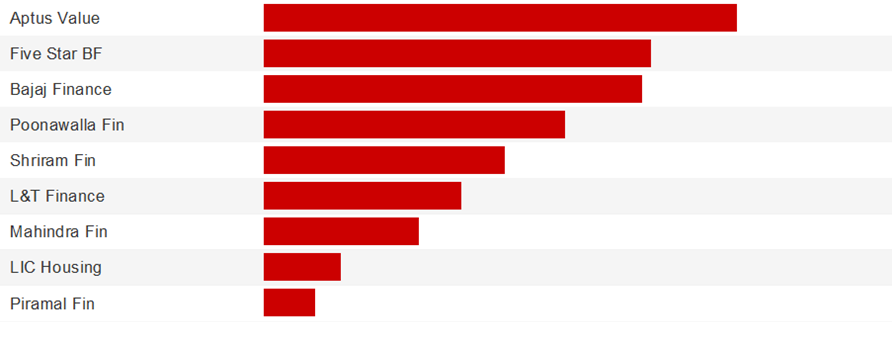

The numbers that matter: cross-sector view

NIMs, and hence ROAs, vary significantly across the NBFC landscape. The following comparisons are instructive for anyone trying to understand which business models generate the most value per unit of risk taken.

Net Interest Margin Comparison Across NBFCs (%)

Source: Company data

Return on Assets: The Ultimate Quality Metric (%)

Source: Company data

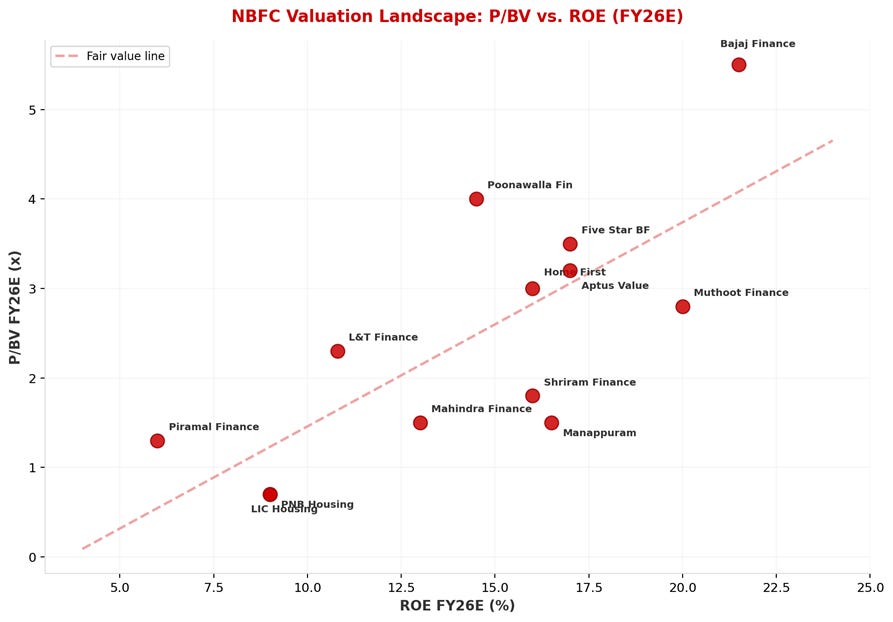

NBFC Valuation Landscape: P/BV vs. ROE (FY26E)

Source: Company data, Bloomberg

This scatter plot deserves attention. The companies above the regression line are trading at a premium to what their current ROE justifies, implying the market is pricing in improvement. Companies below the line are either undervalued or the market is pricing in deterioration. For investors, the bottom-right quadrant (high ROE, low P/BV) is where you find the most interesting opportunities.

Technology: The real differentiator

If there’s one theme that cuts across every NBFC management commentary this earnings season, it’s technology. But the quality of technology investment varies enormously.

At one end: L&T Finance’s Cyclops and Nostradamus AI engines, purpose-built systems demonstrably improving underwriting outcomes. At the other end, companies are spending crores on Salesforce implementations that add cost without meaningfully improving risk selection.

Aptus’s approach is instructive. They use Novac’s LOS (on the same platform Shriram uses) at a fraction of what competitors pay for Salesforce. Asset quality metrics are best-in-class. The lesson: in lending, technology should serve the underwriting process. The fanciest tech stack in the world is worthless if it doesn’t improve your ability to separate good credit risk from bad.

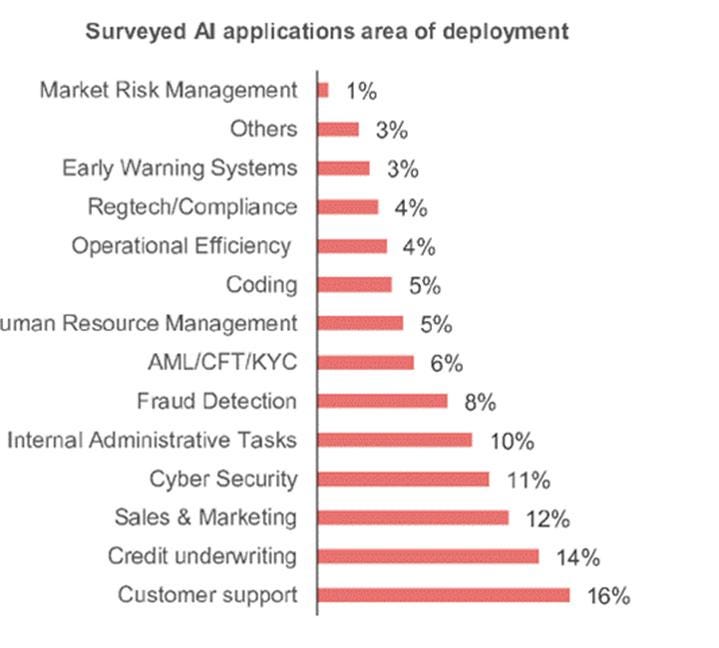

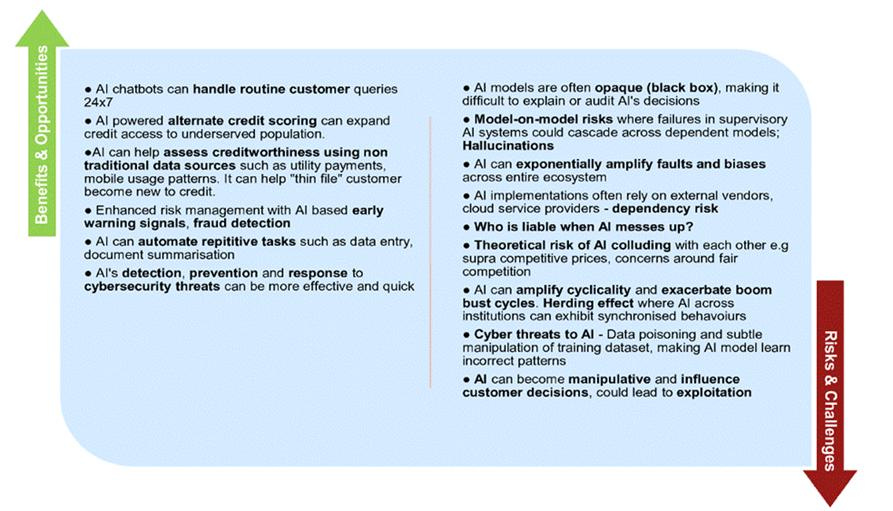

Surveyed AI Applications: Area of Deployment in Financial Services

Source: RBI Survey

I think there is a lot of value to be captured by AI-focused B2B infrastructure players, if they can capture high-value tasks like early warning systems and risk management. The companies building the picks-and-shovels for NBFC AI adoption are, in many ways, the most interesting investment opportunities in the space.

Separately, the Account Aggregator framework, unique to India, gives NBFCs a data advantage that lenders in most other markets don’t have. Companies from AU SFB to LTF to Five Star are integrating AA data into credit decisioning, potentially transforming underwriting for thin-file borrowers. AA-consented data flows are projected to reach 10 billion annually by 2026, up from 1.8 billion in 2024. That is a tenfold increase in the availability of underwriting-grade data in two years.

The Pros and Cons of AI Adoption in Financial Services (RBI Assessment)

Source: RBI

The regulatory landscape and the rate cycle

The RBI’s scale-based regulation framework (Base Layer, Middle Layer, Upper Layer, and Top Layer) has brought the largest NBFCs closer to bank-level regulation. The tightening of personal loan norms in late 2024 and MFI guardrails in 2024-25 have already dampened growth in affected segments.

The RBI’s 25 bps repo rate cut in February 2026 is flowing through unevenly. Companies with higher proportions of floating-rate borrowings see faster transmission. The net effect for most NBFCs is a modest 10-15 bps reduction in the cost of funds over 2-3 quarters. Real beneficiaries will be those entering the rate cycle with higher-yielding products (gold loans, micro-LAP, SME) that offset margin compression.

One development worth watching: the RBI’s Expected Credit Loss (ECL) framework transition, which could require additional provisioning, particularly for smaller private banks and PSU banks. NBFCs that have already built conservative provision buffers (like Shriram, with its robust PCR) will navigate this transition more smoothly.

Capital, governance, and ESG

Capital adequacy across the sector ranges from 16% to 20% CRAR. The sweet spot for leverage is ~5-6x equity. The AA+ to AAA credit rating migration can reduce borrowing costs by 30-50 bps, a massive delta that flows directly to the bottom line.

Governance quality is uneven. The IL&FS and DHFL crises were, at their core, governance failures. The best-governed NBFCs share professionally managed boards, transparent disclosure, and a willingness to moderate growth when risk-reward deteriorates. L&T Finance holds a CRISIL ESG Score of 70 (’Strong’), MSCI ESG rating of ‘A’, and a low risk score from Sustainalytics. ESG is increasingly becoming a capital access criterion as global investors screen for governance quality.

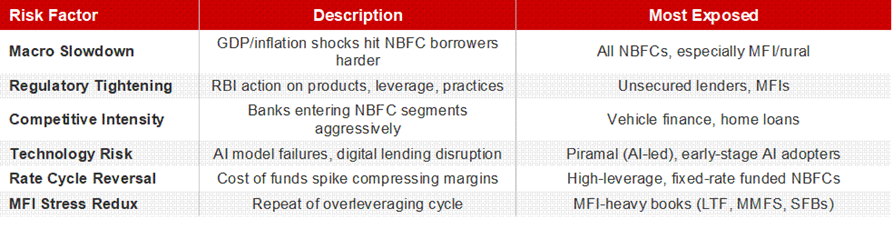

What could go wrong? The risk landscape

Key Risk Matrix for Indian NBFCs

Source: Author’s analysis

The money behind the money: VC, PE, and early-stage investing in NBFCs

Some of the most consequential bets in the Indian NBFC sector were made long before these companies showed up in brokerage reports or on public exchanges. India ranked third globally in fintech funding in 2025, pulling in roughly $2.4 billion, trailing only the US and UK.

Early-stage funding surged 78% year-on-year to $1.2 billion in 2025, up from $667 million in 2024. Even as late-stage cheques got harder to come by (late-stage fintech funding dropped 41% in H1 2025 versus H1 2024), seed and Series A investors were doubling down on the next generation of lending startups. The lending-tech vertical alone absorbed $1.7 billion, or 68% of total fintech funding, in 2024.

India Fintech VC Funding Snapshot (2020-2025)

Source: Industry reports, Tracxn, Inc42

The PE playbook in Indian financial services has been equally aggressive. Financial services investments grew roughly 25% in 2024, driven by renewed interest in affordable housing finance, LAP solutions, and MSME lending. Blackstone, Advent International, and Warburg Pincus were all reportedly evaluating Axis Finance (AUM of Rs 36,962 crore), a deal that could value the platform at approximately $1 billion. DMI Finance, backed by MUFG and Sumitomo Mitsui Trust Bank, has raised $734 million in total funding, with revenue touching Rs 3,180 crore in FY25.

Consolidation accelerated as late-stage funding dried up. Fullerton Financial Holdings acquired a controlling stake in Lendingkart with an additional Rs 252 crore investment in October 2024. InCred Money acquired discount broking platform Stocko. The stronger, better-capitalized players absorb the weaker ones, and the industry structure tightens.

Around 58% of new VC/PE funds launched in 2025 targeted early-stage startups, and fintech accounted for roughly 16% of the total corpus. Given India’s $12.1 billion in new fund launches during 2025, that translates to nearly $2 billion in dry powder earmarked for fintech and financial services.

The smart money is positioning for the next cycle.

The IPO wave: NBFCs go public

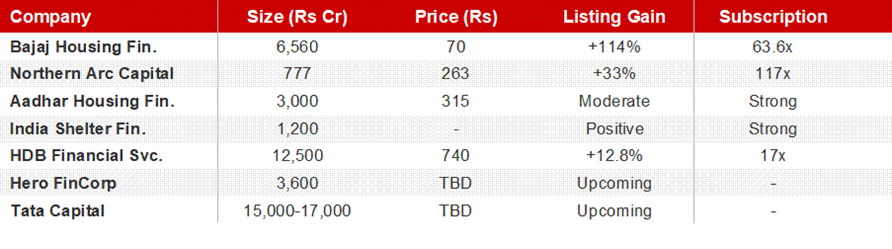

The RBI, in a September 2023 circular, mandated that all ‘upper layer’ NBFCs must list by September 30, 2025. This regulatory push created a forcing function that dragged some of the largest private NBFCs toward the public markets. The result is encouraging: NBFCs raised Rs 635 billion across 24 IPOs in 2025, accounting for a staggering 26.6% of total IPO proceeds for the year. No other sector came close.

Major NBFC IPOs (2024-25)

Source: BSE, NSE, SEBI filings, Chittorgarh.com

The marquee listing of 2024 was undoubtedly Bajaj Housing Finance, which launched its Rs 6,560 crore IPO at Rs 70 per share, listed at Rs 150 (a 114% listing gain), and was subscribed 63.6 times overall with QIBs at 209x. For a housing finance company, those are extraordinary demand metrics. The message was unambiguous: investors are willing to pay premium valuations for well-governed, well-capitalized NBFCs with strong parentage.

HDB Financial Services launched its Rs 12,500 crore IPO in June 2025, subscribed nearly 17 times, and listed at a 12.8% premium. Tata Capital received SEBI’s approval with the offering expected to raise Rs 15,000-17,000 crore. With a consolidated loan book of Rs 1,577 billion (up 35% YoY) and a record PAT of Rs 3,100 crore in FY24, Tata Capital’s listing will likely be one of the biggest IPOs of 2025.

Bajaj Housing Finance IPO: Subscription by Category (times)

Source: BSE data

The pipeline beyond these mega-listings is equally rich. Avanse Financial Services (education financing) filed its DRHP for a Rs 3,500 crore IPO. Moneyview and KreditBee have filed DRHPs (covered in detail in Episode 76). These represent the next tier of specialized NBFCs transitioning from private to public capital.

There are three implications of this IPO wave. First, transparency (public listing forces disclosure and accountability). Second, access to a permanent equity funding channel that reduces dependence on PE/VC. Third, valuation benchmarking (more listed NBFCs means better comparables and more informed capital allocation across the sector).

The risk is that the regulatory-mandated rush pushes some companies public before they’ve built the governance infrastructure that public investors deserve.

The digital-native cohort: bridging the old and new

The Moneyview DRHP, which I covered earlier, has effectively opened the public market template for digital-native lending platforms. But there is a broader cohort of digital NBFCs that sits between the traditional listed NBFCs and the early-stage lending startups. These companies deserve attention because they represent the future competitive landscape for both the traditional players described above and for each other.

KreditBee, India’s second-largest digital personal lender by AUM, posted net profit of INR 473 crore in FY25 on revenue of INR 2,712 crore. Fibe (formerly EarlySalary) has remained profitable for four consecutive years and raised USD 35 million from IFC in December 2025. Kissht filed its own DRHP in August 2025 to raise INR 1,000 crore. Slice completed its landmark merger with North East Small Finance Bank, becoming the first Indian fintech to convert into a banking entity.

And then there’s Zype, a portfolio company at UNLEASH Capital, which achieved profitability in November 2024, just 19 months after launch. Every comparable platform took longer: KreditBee took 3 years, Fibe 7 years, Moneyview 8 years. The playbook is getting compressed because later entrants learn from the mistakes and infrastructure built by earlier ones.

The key question for investors evaluating this cohort is that can you build a profitable digital NBFC at scale, without physical infrastructure? Can AI/ML-based underwriting genuinely outperform bureau-led models through a full credit cycle? The next 2-3 years will answer these questions definitively, and the Moneyview IPO will establish the initial pricing template.

The banking license question: Should NBFCs make the leap?

An important strategic question hangs over the largest NBFCs: should they pursue banking licenses?

The argument for conversion is compelling on paper. A banking license unlocks access to CASA deposits, the cheapest source of funding in financial services. It provides a payment franchise. It elevates brand perception and trust. Bajaj Finance has been rumoured to be considering a banking license for years. AU Small Finance Bank successfully transitioned from an NBFC to an SFB, and its CASA ratio of 35%+ has materially lowered its funding costs relative to its NBFC origins.

The argument against is equally powerful. Banking regulation is significantly more onerous than NBFC regulation: CRR, SLR, PSL mandates, branching requirements, and restrictions on promoter shareholding. The transition period is disruptive. And the NBFC model’s flexibility in product design, pricing, and geographic focus would be constrained under the banking framework.

Slice’s merger with NE SFB is the most recent data point. The integration is complex, the regulatory transition is time-consuming, and the jury is still out on whether the combined entity will deliver better economics than Slice would have as a standalone NBFC.

My view is that for most NBFCs, the co-lending and securitization frameworks have reduced the funding cost disadvantage enough that the marginal benefit of a banking license doesn’t justify the regulatory burden. The exception would be a mega-NBFC like Bajaj Finance, where the CASA opportunity is large enough to be transformative.

The decade ahead: three transitions that will define winners

The Indian NBFC sector is entering what may prove to be its most transformative decade. The companies that thrive will manage three transitions simultaneously.

From volume to quality.

The era of growth-at-all-costs is ending. Regulatory scrutiny, capital constraints, and rising competition mean NBFCs can no longer grow indiscriminately. Winners will demonstrate consistent asset quality through cycles. The MFI crisis of 2024-25 is a recent reminder: the companies that grew fastest during the boom (Fusion, Spandana) suffered the most when the cycle turned. The ones that imposed discipline on themselves (LTF with its three-lender cap, Five Star with its conservative LTVs) came through with portfolios intact. In the NBFC world, the best offense is a good defense. Investors should weigh asset quality consistency at least as heavily as AUM growth when evaluating these businesses.

From physical to phygital.

Pure physical models are expensive: the cost of a branch, a field officer, a vehicle for inspections adds up to Rs 30-50 lakh per branch per year. Pure digital models lack the ground-level intelligence needed to assess collateral in affordable housing, inspect vehicles, or understand local market dynamics. The ‘phygital’ model, combining digital origination and monitoring with physical verification where it matters, is the winning formula. Aptus’s field-based income assessment, combined with digital disbursement, is an example. Shriram’s branch network, supplemented by app-based customer engagement, is another. The companies that get this balance right will have both the reach of digital and the underwriting accuracy of physical.

From mono-product to platform.

L&T Finance’s wholesale-to-retail transformation, Shriram’s post-merger multi-product offering, Manappuram’s diversification beyond gold, and Bajaj Finance’s ecosystem approach all reflect this trend. The logic is straightforward: customer acquisition is expensive, so monetizing each acquired customer across multiple products is the path to higher ROE. The companies that build genuine cross-sell engines (where a gold loan customer becomes a housing loan customer, who becomes an insurance buyer) will compound more durably than single-product lenders.

The sector’s macro tailwinds remain powerful: India’s credit-to-GDP ratio of ~55% is well below peer countries (China at ~180%, the US at ~230%), household leverage is low, financial inclusion is expanding, and the addressable market for formal credit is growing every year. The opportunity is enormous. The question is which companies will capture it, and at what cost to their balance sheets.

For anyone trying to understand Indian finance, the NBFC sector is the single best window into how credit actually works in a developing economy. It’s messy, complex, cyclical, and endlessly fascinating. The numbers are important, and I’ve tried to provide as many as I could in this piece. The stories behind the numbers are what make this sector worth studying.

And the story, right now, is about transformation at every level: from wholesale to retail, from physical to digital, from single-product to platform, from opaque to transparent. The challengers are challenging. The incumbents are adapting. And the next chapter is being written in real time.

Note: This article is for informational purposes only and does not constitute investment advice. Always conduct your own due diligence before making investment decisions.

Disclaimer: The views presented here are my own and don’t reflect the views of my employer in any way, and they shouldn’t be construed as such in any way whatsoever.

Good overview. No mention of Chola?